Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Kellogg Company (NYSE:K) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

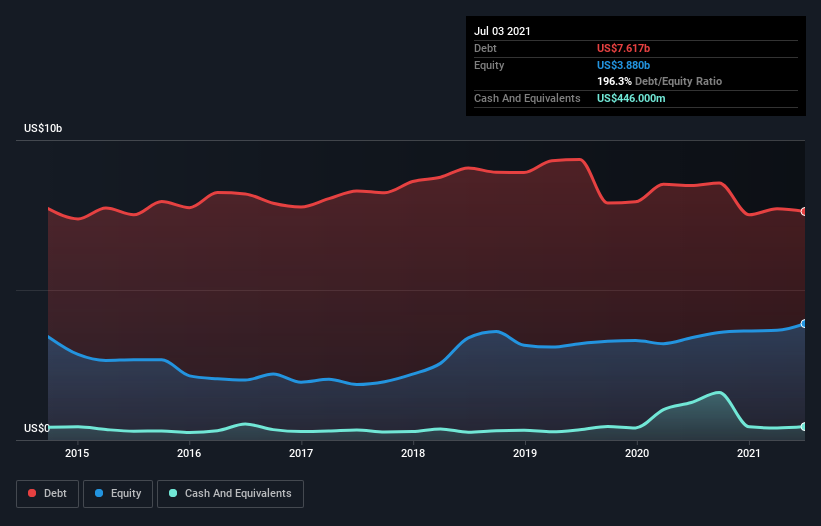

What Is Kellogg’s Net Debt?

As you can see below, Kellogg had US$7.62b of debt at July 2021, down from US$8.48b a year prior. However, it also had US$446.0m in cash, and so its net debt is US$7.17b.

How Healthy Is Kellogg’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Kellogg had liabilities of US$4.95b due within 12 months and liabilities of US$9.39b due beyond that. Offsetting these obligations, it had cash of US$446.0m as well as receivables valued at US$1.66b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$12.2b.

This deficit isn’t so bad because Kellogg is worth a massive US$21.6b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Kellogg has net debt to EBITDA of 3.0 suggesting it uses a fair bit of leverage to boost returns. But the high interest coverage of 7.9 suggests it can easily service that debt. One way Kellogg could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 12%, as it did over the last year. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Kellogg’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Kellogg recorded free cash flow worth 59% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Kellogg’s interest cover was a real positive on this analysis, as was its EBIT growth rate. Having said that, its net debt to EBITDA somewhat sensitizes us to potential future risks to the balance sheet. When we consider all the factors mentioned above, we do feel a bit cautious about Kellogg’s use of debt. While we appreciate debt can enhance returns on equity, we’d suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt.