Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Silgan Holdings Inc. (NASDAQ:SLGN) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Silgan Holdings’s Debt?

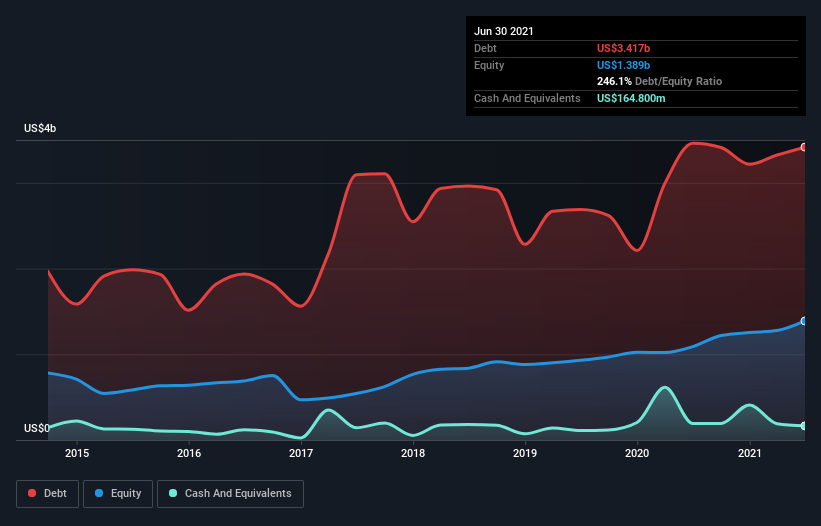

As you can see below, Silgan Holdings had US$3.38b of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. However, it also had US$164.8m in cash, and so its net debt is US$3.22b.

How Healthy Is Silgan Holdings’ Balance Sheet?

The latest balance sheet data shows that Silgan Holdings had liabilities of US$1.07b due within a year, and liabilities of US$4.26b falling due after that. Offsetting these obligations, it had cash of US$164.8m as well as receivables valued at US$891.8m due within 12 months. So it has liabilities totalling US$4.28b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of US$4.43b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Silgan Holdings has a debt to EBITDA ratio of 3.8 and its EBIT covered its interest expense 5.6 times. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. Also relevant is that Silgan Holdings has grown its EBIT by a very respectable 27% in the last year, thus enhancing its ability to pay down debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Silgan Holdings’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Silgan Holdings recorded free cash flow worth 55% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Neither Silgan Holdings’s ability to handle its total liabilities nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But its EBIT growth rate tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that Silgan Holdings is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start.