Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Amdocs Limited (NASDAQ:DOX) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Amdocs’s Net Debt?

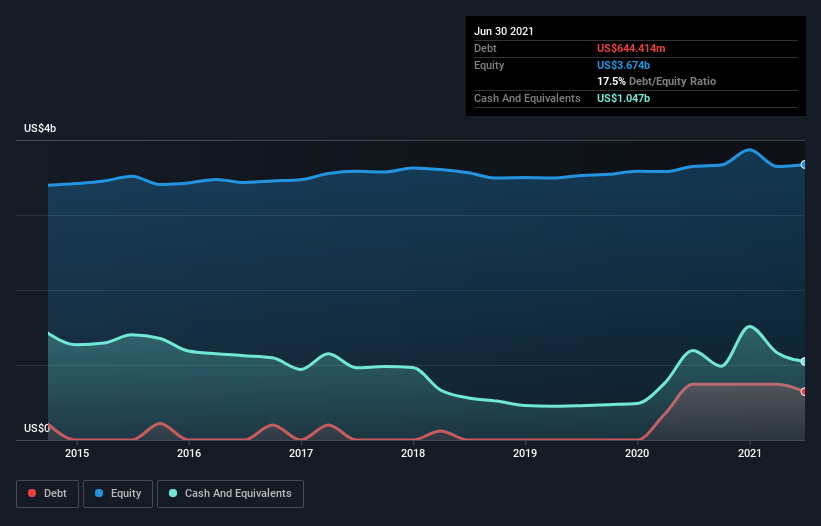

You can click the graphic below for the historical numbers, but it shows that Amdocs had US$644.4m of debt in June 2021, down from US$743.8m, one year before. But it also has US$1.05b in cash to offset that, meaning it has US$402.2m net cash.

How Strong Is Amdocs’ Balance Sheet?

According to the last reported balance sheet, Amdocs had liabilities of US$1.28b due within 12 months, and liabilities of US$1.62b due beyond 12 months. Offsetting this, it had US$1.05b in cash and US$925.1m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$922.0m.

Given Amdocs has a market capitalization of US$9.83b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Amdocs also has more cash than debt, so we’re pretty confident it can manage its debt safely.

While Amdocs doesn’t seem to have gained much on the EBIT line, at least earnings remain stable for now. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Amdocs can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Amdocs has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Amdocs generated free cash flow amounting to a very robust 94% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Summing up

We could understand if investors are concerned about Amdocs’s liabilities, but we can be reassured by the fact it has has net cash of US$402.2m. And it impressed us with free cash flow of US$721m, being 94% of its EBIT. So we don’t think Amdocs’s use of debt is risky. There’s no doubt that we learn most about debt from the balance sheet.