Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Equifax Inc. (NYSE:EFX) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

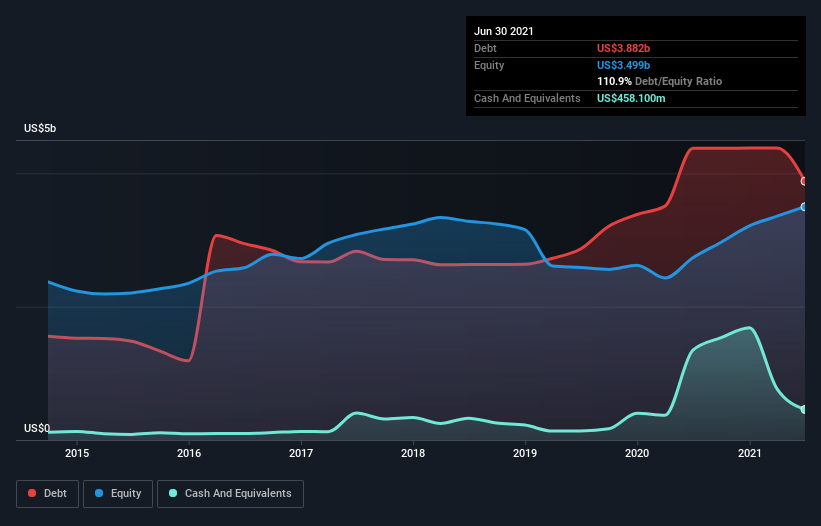

What Is Equifax’s Debt?

As you can see below, Equifax had US$3.88b of debt at June 2021, down from US$4.38b a year prior. However, it also had US$458.1m in cash, and so its net debt is US$3.42b.

How Healthy Is Equifax’s Balance Sheet?

The latest balance sheet data shows that Equifax had liabilities of US$1.88b due within a year, and liabilities of US$3.97b falling due after that. Offsetting these obligations, it had cash of US$458.1m as well as receivables valued at US$694.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.69b.

Given Equifax has a humongous market capitalization of US$33.9b, it’s hard to believe these liabilities pose much threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Equifax’s net debt is sitting at a very reasonable 2.4 times its EBITDA, while its EBIT covered its interest expense just 6.8 times last year. While these numbers do not alarm us, it’s worth noting that the cost of the company’s debt is having a real impact. It is well worth noting that Equifax’s EBIT shot up like bamboo after rain, gaining 68% in the last twelve months. That’ll make it easier to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Equifax’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Equifax’s free cash flow amounted to 45% of its EBIT, less than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

Happily, Equifax’s impressive EBIT growth rate implies it has the upper hand on its debt. And its interest cover is good too. All these things considered, it appears that Equifax can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it’s worth monitoring the balance sheet. There’s no doubt that we learn most about debt from the balance sheet.