Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, HireQuest, Inc. (NASDAQ:HQI) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does HireQuest Carry?

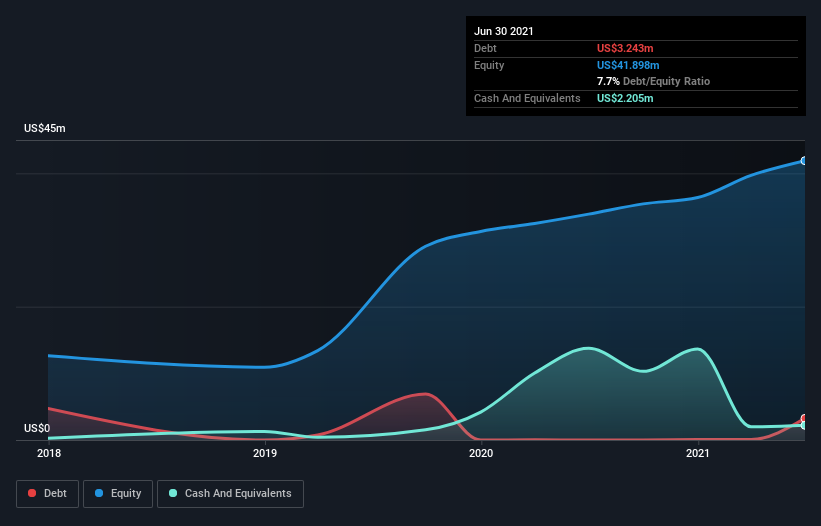

You can click the graphic below for the historical numbers, but it shows that as of June 2021 HireQuest had US$3.24m of debt, an increase on none, over one year. On the flip side, it has US$2.20m in cash leading to net debt of about US$1.04m.

How Healthy Is HireQuest’s Balance Sheet?

The latest balance sheet data shows that HireQuest had liabilities of US$19.7m due within a year, and liabilities of US$8.16m falling due after that. Offsetting this, it had US$2.20m in cash and US$36.6m in receivables that were due within 12 months. So it actually has US$11.0m more liquid assets than total liabilities.

This surplus suggests that HireQuest has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Carrying virtually no net debt, HireQuest has a very light debt load indeed.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

HireQuest has net debt of just 0.11 times EBITDA, suggesting it could ramp leverage without breaking a sweat. But the really cool thing is that it actually managed to receive more interest than it paid, over the last year. So it’s fair to say it can handle debt like a hotshot teppanyaki chef handles cooking. On top of that, HireQuest grew its EBIT by 65% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is HireQuest’s earnings that will influence how the balance sheet holds up in the future. So when considering debt, it’s definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, HireQuest actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

HireQuest’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! We think HireQuest is no more beholden to its lenders, than the birds are to birdwatchers.