Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Fortinet, Inc. (NASDAQ:FTNT) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Fortinet’s Debt?

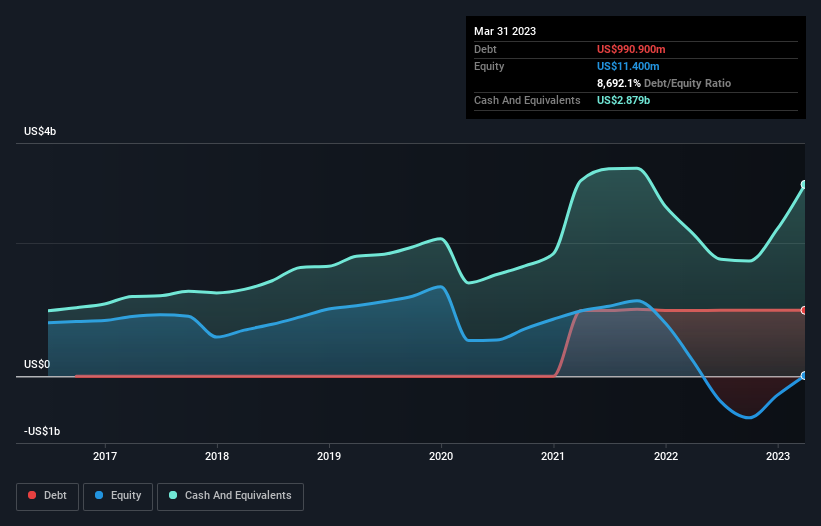

The chart below, which you can click on for greater detail, shows that Fortinet had US$990.9m in debt in March 2023; about the same as the year before. However, its balance sheet shows it holds US$2.88b in cash, so it actually has US$1.89b net cash.

How Healthy Is Fortinet’s Balance Sheet?

We can see from the most recent balance sheet that Fortinet had liabilities of US$3.26b falling due within a year, and liabilities of US$3.56b due beyond that. On the other hand, it had cash of US$2.88b and US$1.09b worth of receivables due within a year. So its liabilities total US$2.85b more than the combination of its cash and short-term receivables.

Of course, Fortinet has a titanic market capitalization of US$50.7b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Fortinet also has more cash than debt, so we’re pretty confident it can manage its debt safely.

On top of that, Fortinet grew its EBIT by 61% over the last twelve months, and that growth will make it easier to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Fortinet can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. Fortinet may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Fortinet actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

While it is always sensible to look at a company’s total liabilities, it is very reassuring that Fortinet has US$1.89b in net cash. The cherry on top was that in converted 173% of that EBIT to free cash flow, bringing in US$1.8b. So is Fortinet’s debt a risk? It doesn’t seem so to us. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all.