Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Matson, Inc. (NYSE:MATX) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Matson’s Debt?

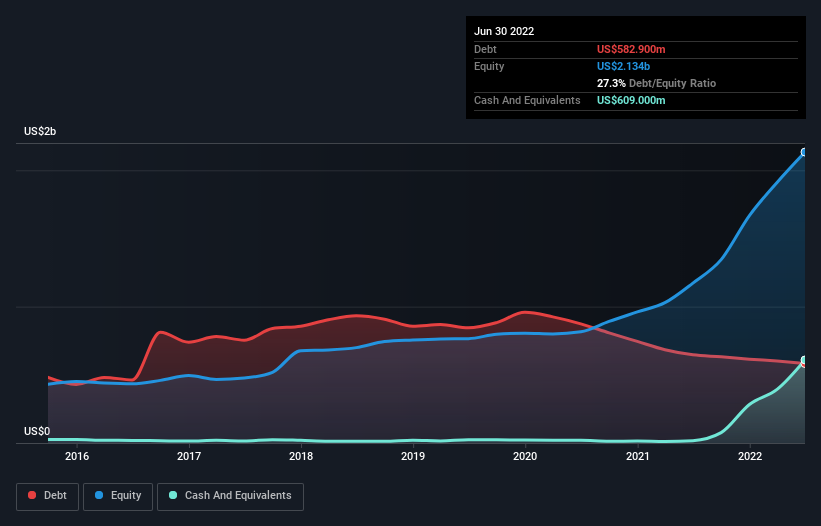

The image below, which you can click on for greater detail, shows that Matson had debt of US$582.9m at the end of June 2022, a reduction from US$646.5m over a year. However, its balance sheet shows it holds US$609.0m in cash, so it actually has US$26.1m net cash.

How Healthy Is Matson’s Balance Sheet?

We can see from the most recent balance sheet that Matson had liabilities of US$632.1m falling due within a year, and liabilities of US$1.39b due beyond that. Offsetting these obligations, it had cash of US$609.0m as well as receivables valued at US$380.6m due within 12 months. So it has liabilities totalling US$1.04b more than its cash and near-term receivables, combined.

Matson has a market capitalization of US$2.83b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, Matson also has more cash than debt, so we’re pretty confident it can manage its debt safely.

Even more impressive was the fact that Matson grew its EBIT by 228% over twelve months. That boost will make it even easier to pay down debt going forward. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Matson can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. While Matson has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, Matson recorded free cash flow worth 60% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing Up

Although Matson’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$26.1m. And it impressed us with its EBIT growth of 228% over the last year. So is Matson’s debt a risk? It doesn’t seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.