Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that The Southern Company (NYSE:SO) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Southern’s Debt?

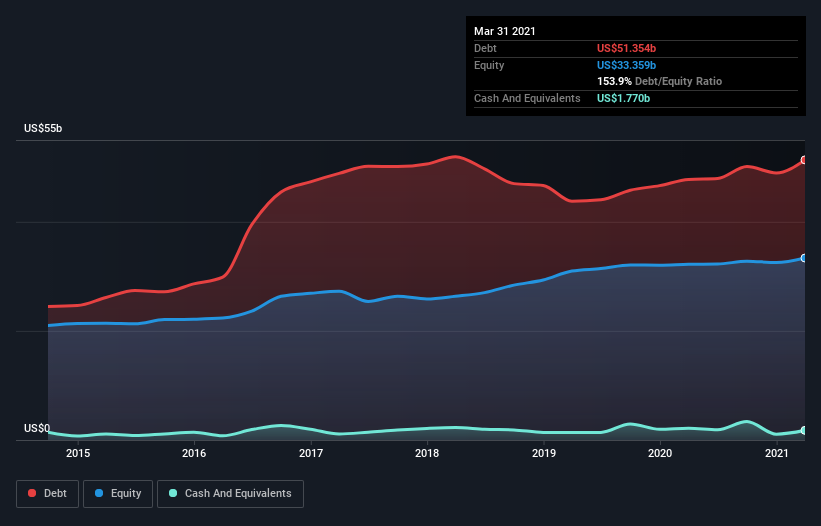

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Southern had US$51.4b of debt, an increase on US$47.8b, over one year. On the flip side, it has US$1.77b in cash leading to net debt of about US$49.6b.

How Strong Is Southern’s Balance Sheet?

We can see from the most recent balance sheet that Southern had liabilities of US$11.6b falling due within a year, and liabilities of US$80.4b due beyond that. Offsetting this, it had US$1.77b in cash and US$3.03b in receivables that were due within 12 months. So its liabilities total US$87.2b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company’s huge US$66.8b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a net debt to EBITDA ratio of 5.2, it’s fair to say Southern does have a significant amount of debt. However, its interest coverage of 3.1 is reasonably strong, which is a good sign. Given the debt load, it’s hardly ideal that Southern’s EBIT was pretty flat over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Southern’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Southern burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Southern’s net debt to EBITDA and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. Having said that, its ability to grow its EBIT isn’t such a worry. We should also note that Electric Utilities industry companies like Southern commonly do use debt without problems. We’re quite clear that we consider Southern to be really rather risky, as a result of its balance sheet health. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they say. When analysing debt levels, the balance sheet is the obvious place to start.