Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies DHT Holdings, Inc. (NYSE:DHT) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does DHT Holdings Carry?

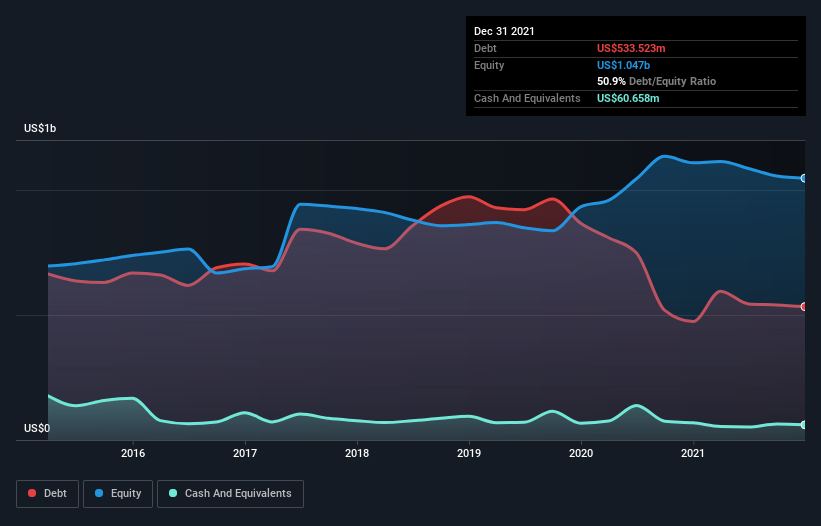

You can click the graphic below for the historical numbers, but it shows that as of December 2021 DHT Holdings had US$533.5m of debt, an increase on US$473.6m, over one year. However, because it has a cash reserve of US$60.7m, its net debt is less, at about US$472.9m.

How Strong Is DHT Holdings’ Balance Sheet?

We can see from the most recent balance sheet that DHT Holdings had liabilities of US$41.9m falling due within a year, and liabilities of US$520.1m due beyond that. Offsetting these obligations, it had cash of US$60.7m as well as receivables valued at US$30.4m due within 12 months. So its liabilities total US$471.0m more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since DHT Holdings has a market capitalization of US$946.9m, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine DHT Holdings’s ability to maintain a healthy balance sheet going forward.

Over 12 months, DHT Holdings made a loss at the EBIT level, and saw its revenue drop to US$296m, which is a fall of 57%. That makes us nervous, to say the least.

Caveat Emptor

Not only did DHT Holdings’s revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost US$20m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled US$114m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky.