Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that SpartanNash Company (NASDAQ:SPTN) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is SpartanNash’s Debt?

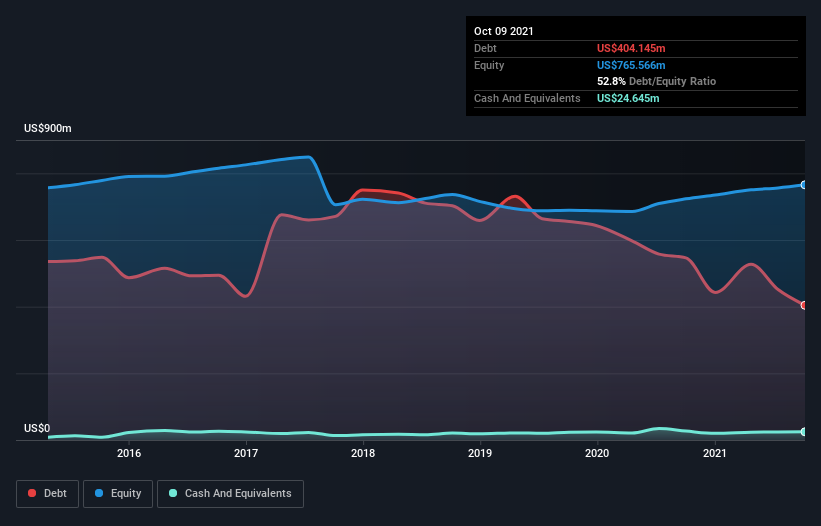

You can click the graphic below for the historical numbers, but it shows that SpartanNash had US$404.1m of debt in October 2021, down from US$546.3m, one year before. On the flip side, it has US$24.6m in cash leading to net debt of about US$379.5m.

A Look At SpartanNash’s Liabilities

Zooming in on the latest balance sheet data, we can see that SpartanNash had liabilities of US$702.0m due within 12 months and liabilities of US$775.1m due beyond that. On the other hand, it had cash of US$24.6m and US$372.0m worth of receivables due within a year. So it has liabilities totalling US$1.08b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company’s market capitalization of US$920.9m, we think shareholders really should watch SpartanNash’s debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With a debt to EBITDA ratio of 1.9, SpartanNash uses debt artfully but responsibly. And the alluring interest cover (EBIT of 7.1 times interest expense) certainly does not do anything to dispel this impression. The bad news is that SpartanNash saw its EBIT decline by 15% over the last year. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if SpartanNash can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, SpartanNash actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Neither SpartanNash’s ability to grow its EBIT nor its level of total liabilities gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. Taking the abovementioned factors together we do think SpartanNash’s debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start.