Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Magnolia Oil & Gas Corporation (NYSE:MGY) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Magnolia Oil & Gas’s Net Debt?

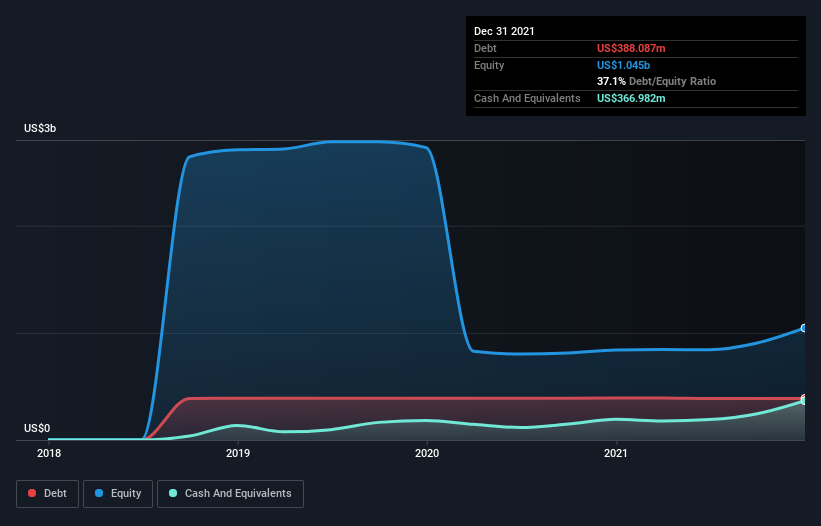

The chart below, which you can click on for greater detail, shows that Magnolia Oil & Gas had US$388.1m in debt in December 2021; about the same as the year before. However, it also had US$367.0m in cash, and so its net debt is US$21.1m.

How Strong Is Magnolia Oil & Gas’ Balance Sheet?

The latest balance sheet data shows that Magnolia Oil & Gas had liabilities of US$218.5m due within a year, and liabilities of US$482.9m falling due after that. Offsetting these obligations, it had cash of US$367.0m as well as receivables valued at US$149.8m due within 12 months. So it has liabilities totalling US$184.7m more than its cash and near-term receivables, combined.

Given Magnolia Oil & Gas has a market capitalization of US$4.94b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Carrying virtually no net debt, Magnolia Oil & Gas has a very light debt load indeed.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With debt at a measly 0.026 times EBITDA and EBIT covering interest a whopping 19.4 times, it’s clear that Magnolia Oil & Gas is not a desperate borrower. Indeed relative to its earnings its debt load seems light as a feather. It was also good to see that despite losing money on the EBIT line last year, Magnolia Oil & Gas turned things around in the last 12 months, delivering and EBIT of US$599m. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Magnolia Oil & Gas’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. During the last year, Magnolia Oil & Gas generated free cash flow amounting to a very robust 92% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

Magnolia Oil & Gas’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. Looking at the bigger picture, we think Magnolia Oil & Gas’s use of debt seems quite reasonable and we’re not concerned about it. While debt does bring risk, when used wisely it can also bring a higher return on equity. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.