Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that NXP Semiconductors N.V. (NASDAQ:NXPI) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is NXP Semiconductors’s Net Debt?

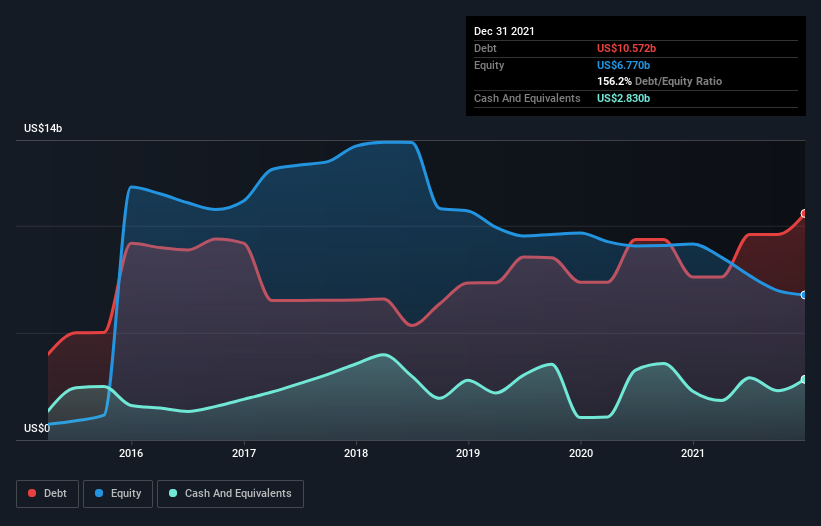

As you can see below, at the end of December 2021, NXP Semiconductors had US$10.6b of debt, up from US$7.61b a year ago. Click the image for more detail. However, it does have US$2.83b in cash offsetting this, leading to net debt of about US$7.74b.

A Look At NXP Semiconductors’ Liabilities

The latest balance sheet data shows that NXP Semiconductors had liabilities of US$2.45b due within a year, and liabilities of US$11.6b falling due after that. On the other hand, it had cash of US$2.83b and US$923.0m worth of receivables due within a year. So it has liabilities totalling US$10.3b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since NXP Semiconductors has a huge market capitalization of US$46.3b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

NXP Semiconductors’s net debt of 2.0 times EBITDA suggests graceful use of debt. And the fact that its trailing twelve months of EBIT was 7.1 times its interest expenses harmonizes with that theme. Notably, NXP Semiconductors’s EBIT launched higher than Elon Musk, gaining a whopping 533% on last year. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if NXP Semiconductors can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, NXP Semiconductors actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

The good news is that NXP Semiconductors’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. Zooming out, NXP Semiconductors seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. The balance sheet is clearly the area to focus on when you are analysing debt.