Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, GATX Corporation (NYSE:GATX) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is GATX’s Debt?

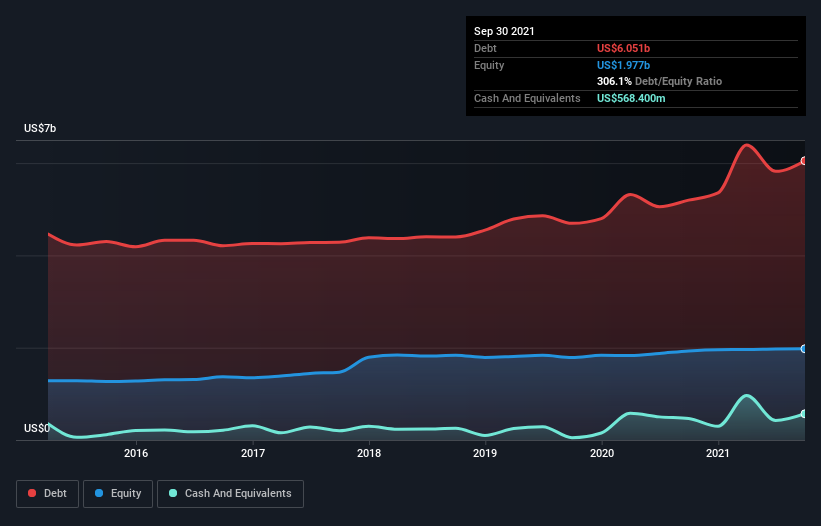

The image below, which you can click on for greater detail, shows that at September 2021 GATX had debt of US$6.05b, up from US$5.20b in one year. However, because it has a cash reserve of US$568.4m, its net debt is less, at about US$5.48b.

A Look At GATX’s Liabilities

According to the last reported balance sheet, GATX had liabilities of US$193.3m due within 12 months, and liabilities of US$7.42b due beyond 12 months. On the other hand, it had cash of US$568.4m and US$140.3m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$6.90b.

This deficit casts a shadow over the US$3.60b company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. At the end of the day, GATX would probably need a major re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 1.5 times and a disturbingly high net debt to EBITDA ratio of 8.2 hit our confidence in GATX like a one-two punch to the gut. This means we’d consider it to have a heavy debt load. Fortunately, GATX grew its EBIT by 9.9% in the last year, slowly shrinking its debt relative to earnings. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if GATX can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, GATX saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, GATX’s conversion of EBIT to free cash flow left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least it’s pretty decent at growing its EBIT; that’s encouraging. After considering the datapoints discussed, we think GATX has too much debt. That sort of riskiness is ok for some, but it certainly doesn’t float our boat. The balance sheet is clearly the area to focus on when you are analysing debt.