Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Lazydays Holdings, Inc. (NASDAQ:LAZY) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Lazydays Holdings’s Debt?

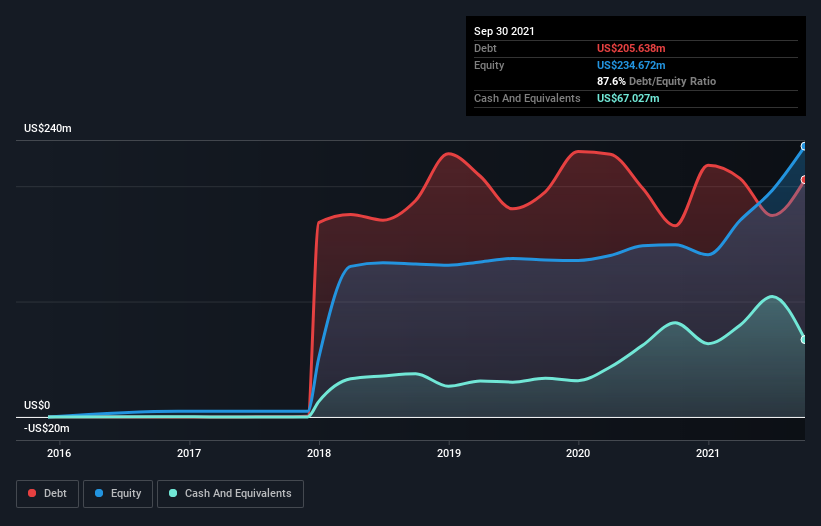

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Lazydays Holdings had US$205.6m of debt, an increase on US$165.7m, over one year. However, it also had US$67.0m in cash, and so its net debt is US$138.6m.

How Healthy Is Lazydays Holdings’ Balance Sheet?

We can see from the most recent balance sheet that Lazydays Holdings had liabilities of US$170.5m falling due within a year, and liabilities of US$157.1m due beyond that. Offsetting these obligations, it had cash of US$67.0m as well as receivables valued at US$31.0m due within 12 months. So it has liabilities totalling US$229.6m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of US$238.2m, so it does suggest shareholders should keep an eye on Lazydays Holdings’ use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Lazydays Holdings’s net debt is only 1.1 times its EBITDA. And its EBIT covers its interest expense a whopping 14.7 times over. So we’re pretty relaxed about its super-conservative use of debt. Better yet, Lazydays Holdings grew its EBIT by 201% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Lazydays Holdings’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Lazydays Holdings generated free cash flow amounting to a very robust 99% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that Lazydays Holdings’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But we must concede we find its level of total liabilities has the opposite effect. When we consider the range of factors above, it looks like Lazydays Holdings is pretty sensible with its use of debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. There’s no doubt that we learn most about debt from the balance sheet.