Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Townsquare Media, Inc. (NYSE:TSQ) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Townsquare Media’s Debt?

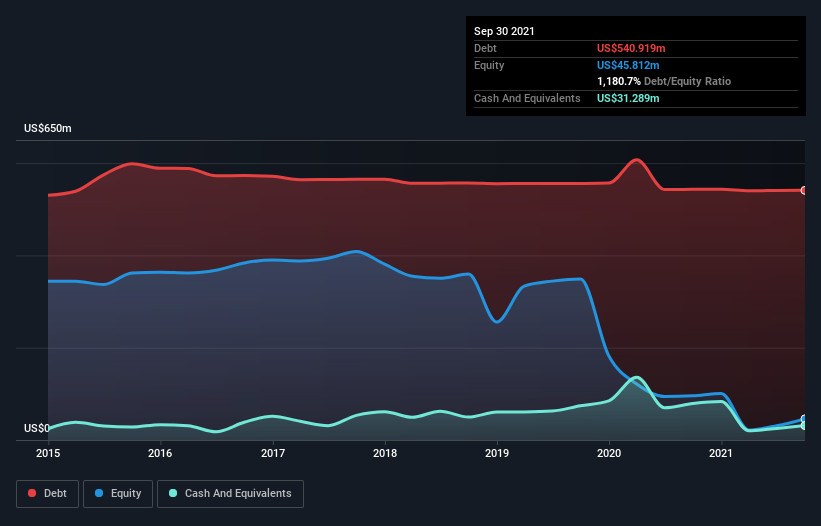

As you can see below, Townsquare Media had US$540.9m of debt, at September 2021, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$31.3m, its net debt is less, at about US$509.6m.

How Strong Is Townsquare Media’s Balance Sheet?

According to the last reported balance sheet, Townsquare Media had liabilities of US$64.7m due within 12 months, and liabilities of US$601.0m due beyond 12 months. On the other hand, it had cash of US$31.3m and US$57.9m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$576.6m.

This deficit casts a shadow over the US$211.9m company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Townsquare Media would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While we wouldn’t worry about Townsquare Media’s net debt to EBITDA ratio of 4.9, we think its super-low interest cover of 2.2 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. The silver lining is that Townsquare Media grew its EBIT by 128% last year, which nourishing like the idealism of youth. If that earnings trend continues it will make its debt load much more manageable in the future. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Townsquare Media can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. In the last three years, Townsquare Media’s free cash flow amounted to 43% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Our View

We’d go so far as to say Townsquare Media’s level of total liabilities was disappointing. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that Townsquare Media’s use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. The balance sheet is clearly the area to focus on when you are analysing debt.