Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Marathon Oil Corporation (NYSE:MRO) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Marathon Oil’s Net Debt?

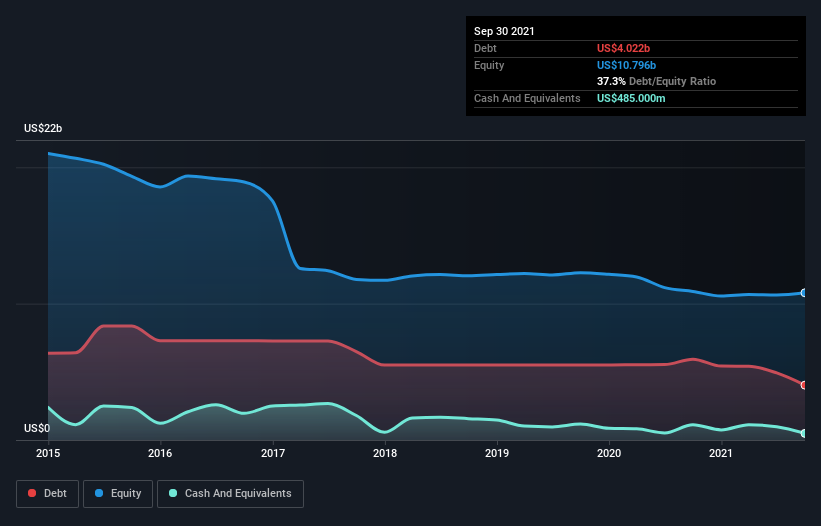

You can click the graphic below for the historical numbers, but it shows that Marathon Oil had US$4.02b of debt in September 2021, down from US$5.93b, one year before. On the flip side, it has US$485.0m in cash leading to net debt of about US$3.54b.

A Look At Marathon Oil’s Liabilities

We can see from the most recent balance sheet that Marathon Oil had liabilities of US$1.68b falling due within a year, and liabilities of US$4.69b due beyond that. On the other hand, it had cash of US$485.0m and US$1.07b worth of receivables due within a year. So it has liabilities totalling US$4.81b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Marathon Oil has a huge market capitalization of US$12.5b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Given net debt is only 1.4 times EBITDA, it is initially surprising to see that Marathon Oil’s EBIT has low interest coverage of 0.92 times. So one way or the other, it’s clear the debt levels are not trivial. We also note that Marathon Oil improved its EBIT from a last year’s loss to a positive US$181m. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Marathon Oil can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, Marathon Oil actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Based on what we’ve seen Marathon Oil is not finding it easy, given its interest cover, but the other factors we considered give us cause to be optimistic. In particular, we are dazzled with its conversion of EBIT to free cash flow. Considering this range of data points, we think Marathon Oil is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There’s no doubt that we learn most about debt from the balance sheet.