Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Western Digital Corporation (NASDAQ:WDC) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Western Digital’s Debt?

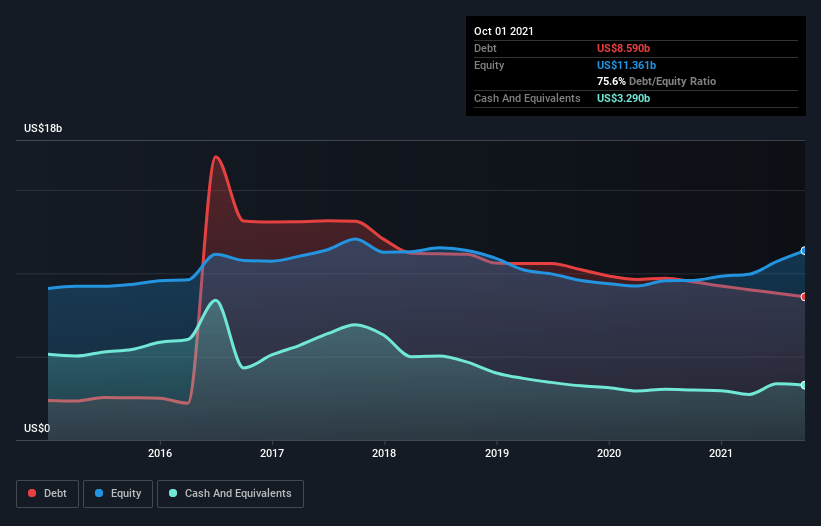

You can click the graphic below for the historical numbers, but it shows that Western Digital had US$8.59b of debt in October 2021, down from US$9.49b, one year before. However, because it has a cash reserve of US$3.29b, its net debt is less, at about US$5.30b.

How Healthy Is Western Digital’s Balance Sheet?

The latest balance sheet data shows that Western Digital had liabilities of US$4.71b due within a year, and liabilities of US$10.3b falling due after that. Offsetting this, it had US$3.29b in cash and US$2.45b in receivables that were due within 12 months. So its liabilities total US$9.29b more than the combination of its cash and short-term receivables.

Western Digital has a very large market capitalization of US$17.4b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Western Digital has net debt worth 1.8 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 6.0 times the interest expense. While these numbers do not alarm us, it’s worth noting that the cost of the company’s debt is having a real impact. Pleasingly, Western Digital is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 266% gain in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Western Digital can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent two years, Western Digital recorded free cash flow of 46% of its EBIT, which is weaker than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

On our analysis Western Digital’s EBIT growth rate should signal that it won’t have too much trouble with its debt. But the other factors we noted above weren’t so encouraging. For example, its level of total liabilities makes us a little nervous about its debt. When we consider all the elements mentioned above, it seems to us that Western Digital is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. When analysing debt levels, the balance sheet is the obvious place to start.