The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Zuora, Inc. (NYSE:ZUO) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Zuora Carry?

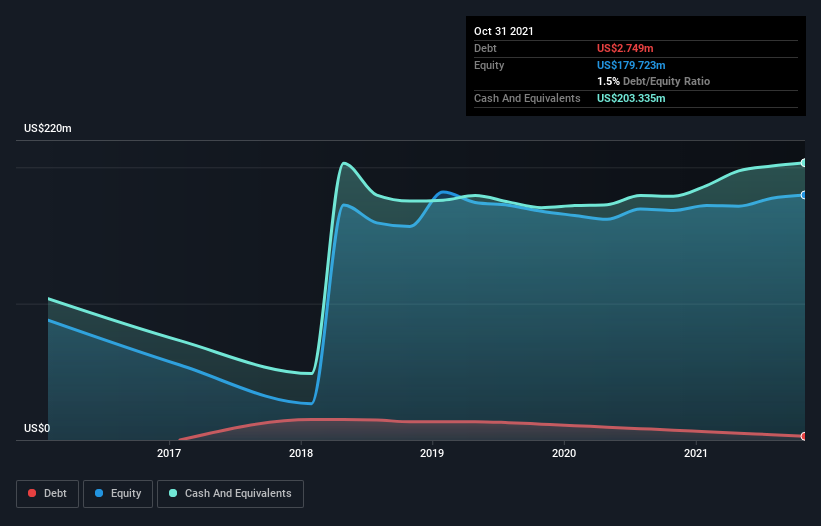

The image below, which you can click on for greater detail, shows that Zuora had debt of US$2.75m at the end of October 2021, a reduction from US$7.22m over a year. However, it does have US$203.3m in cash offsetting this, leading to net cash of US$200.6m.

A Look At Zuora’s Liabilities

According to the last reported balance sheet, Zuora had liabilities of US$195.2m due within 12 months, and liabilities of US$54.3m due beyond 12 months. Offsetting this, it had US$203.3m in cash and US$72.4m in receivables that were due within 12 months. So it can boast US$26.2m more liquid assets than total liabilities.

This state of affairs indicates that Zuora’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it’s very unlikely that the US$2.38b company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, Zuora boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Zuora’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Zuora reported revenue of US$335m, which is a gain of 13%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Zuora?

Although Zuora had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$3.0m. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. With mediocre revenue growth in the last year, we’re don’t find the investment opportunity particularly compelling. There’s no doubt that we learn most about debt from the balance sheet.