Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that The RealReal, Inc. (NASDAQ:REAL) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is RealReal’s Net Debt?

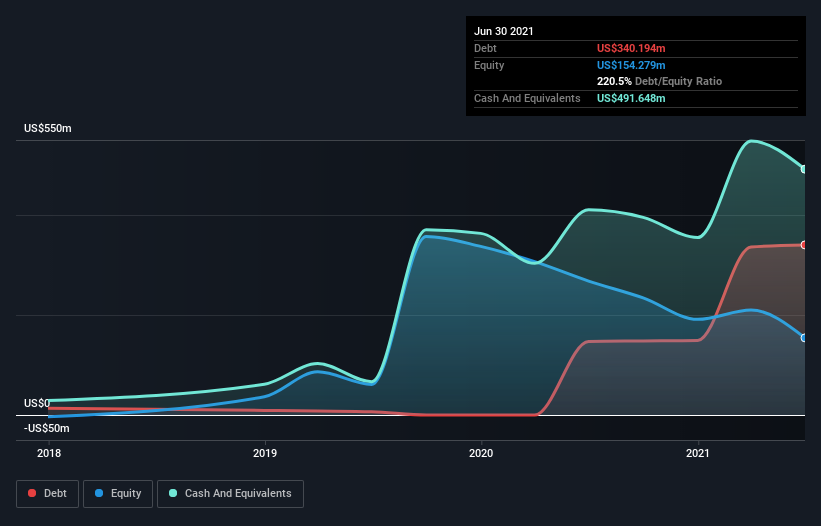

The image below, which you can click on for greater detail, shows that at June 2021 RealReal had debt of US$340.2m, up from US$147.0m in one year. However, its balance sheet shows it holds US$491.6m in cash, so it actually has US$151.5m net cash.

How Healthy Is RealReal’s Balance Sheet?

According to the last reported balance sheet, RealReal had liabilities of US$160.8m due within 12 months, and liabilities of US$481.4m due beyond 12 months. Offsetting these obligations, it had cash of US$491.6m as well as receivables valued at US$5.81m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$144.8m.

Since publicly traded RealReal shares are worth a total of US$1.25b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, RealReal also has more cash than debt, so we’re pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if RealReal can strengthen its balance sheet over time.

Over 12 months, RealReal reported revenue of US$368m, which is a gain of 19%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is RealReal?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months RealReal lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$174m and booked a US$221m accounting loss. However, it has net cash of US$151.5m, so it has a bit of time before it will need more capital. Summing up, we’re a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. The balance sheet is clearly the area to focus on when you are analysing debt.