David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Regal Rexnord Corporation (NYSE:RRX) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Regal Rexnord Carry?

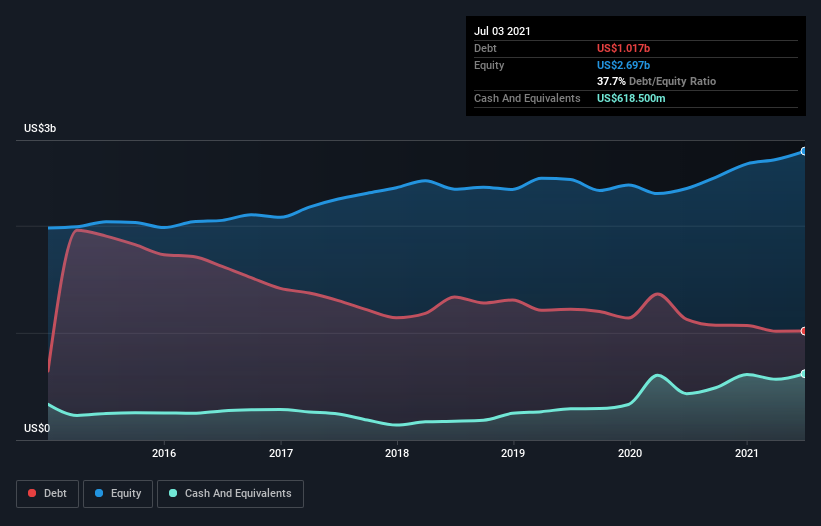

You can click the graphic below for the historical numbers, but it shows that Regal Rexnord had US$1.02b of debt in July 2021, down from US$1.12b, one year before. However, because it has a cash reserve of US$618.5m, its net debt is less, at about US$398.2m.

How Strong Is Regal Rexnord’s Balance Sheet?

We can see from the most recent balance sheet that Regal Rexnord had liabilities of US$938.8m falling due within a year, and liabilities of US$1.14b due beyond that. On the other hand, it had cash of US$618.5m and US$558.0m worth of receivables due within a year. So its liabilities total US$900.7m more than the combination of its cash and short-term receivables.

Since publicly traded Regal Rexnord shares are worth a total of US$9.77b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Regal Rexnord has a low net debt to EBITDA ratio of only 0.73. And its EBIT covers its interest expense a whopping 11.8 times over. So we’re pretty relaxed about its super-conservative use of debt. In addition to that, we’re happy to report that Regal Rexnord has boosted its EBIT by 44%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Regal Rexnord’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Regal Rexnord recorded free cash flow worth a fulsome 91% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Our View

Happily, Regal Rexnord’s impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. It looks Regal Rexnord has no trouble standing on its own two feet, and it has no reason to fear its lenders. To our minds it has a healthy happy balance sheet. The balance sheet is clearly the area to focus on when you are analysing debt.