Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Evoqua Water Technologies Corp. (NYSE:AQUA) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Evoqua Water Technologies’s Debt?

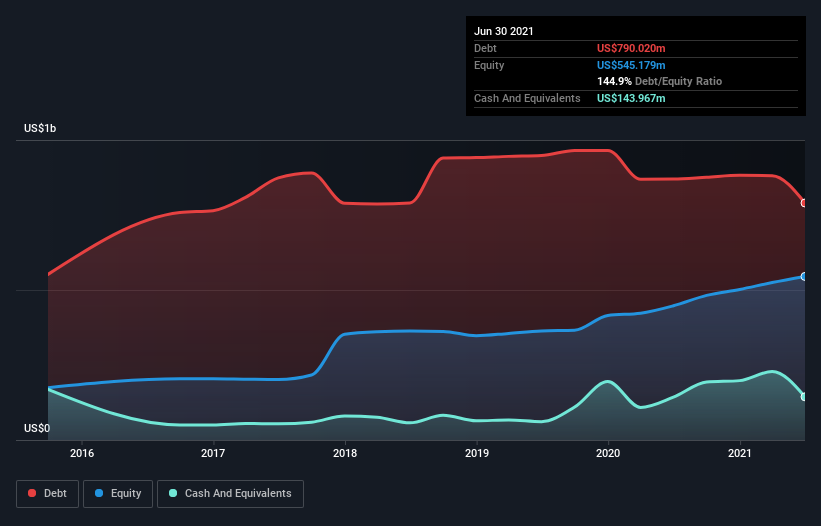

You can click the graphic below for the historical numbers, but it shows that Evoqua Water Technologies had US$790.0m of debt in June 2021, down from US$870.0m, one year before. However, it does have US$144.0m in cash offsetting this, leading to net debt of about US$646.1m.

A Look At Evoqua Water Technologies’ Liabilities

We can see from the most recent balance sheet that Evoqua Water Technologies had liabilities of US$370.7m falling due within a year, and liabilities of US$927.3m due beyond that. On the other hand, it had cash of US$144.0m and US$317.9m worth of receivables due within a year. So it has liabilities totalling US$836.1m more than its cash and near-term receivables, combined.

Of course, Evoqua Water Technologies has a market capitalization of US$4.71b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Evoqua Water Technologies has a debt to EBITDA ratio of 2.8 and its EBIT covered its interest expense 3.2 times. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. More concerning, Evoqua Water Technologies saw its EBIT drop by 8.8% in the last twelve months. If that earnings trend continues the company will face an uphill battle to pay off its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Evoqua Water Technologies’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Evoqua Water Technologies’s free cash flow amounted to 45% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Both Evoqua Water Technologies’s interest cover and its EBIT growth rate were discouraging. At least its level of total liabilities gives us reason to be optimistic. When we consider all the factors discussed, it seems to us that Evoqua Water Technologies is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here.