Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Watsco, Inc. (NYSE:WSO) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

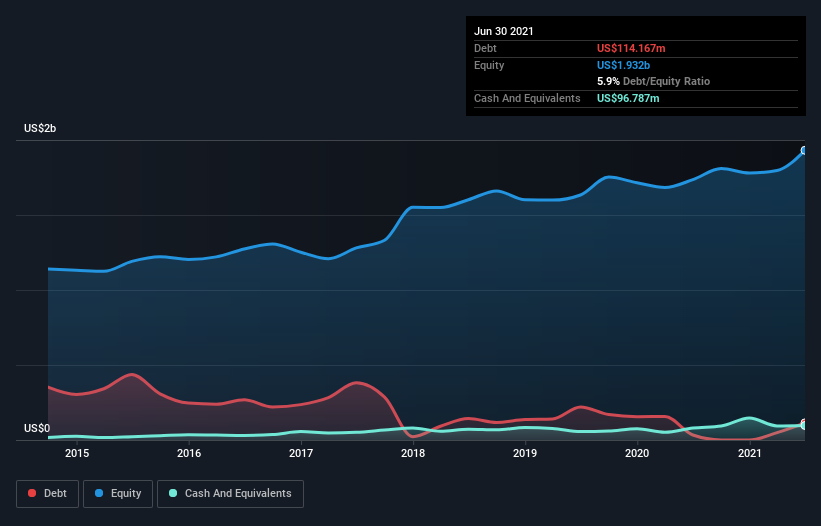

What Is Watsco’s Net Debt?

As you can see below, at the end of June 2021, Watsco had US$114.2m of debt, up from US$33.4m a year ago. Click the image for more detail. However, it does have US$96.8m in cash offsetting this, leading to net debt of about US$17.4m.

A Look At Watsco’s Liabilities

The latest balance sheet data shows that Watsco had liabilities of US$815.3m due within a year, and liabilities of US$384.9m falling due after that. On the other hand, it had cash of US$96.8m and US$857.9m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$245.5m.

Given Watsco has a market capitalization of US$9.75b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. But either way, Watsco has virtually no net debt, so it’s fair to say it does not have a heavy debt load!

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Watsco has very little debt (net of cash), and boasts a debt to EBITDA ratio of 0.032 and EBIT of 727 times the interest expense. So relative to past earnings, the debt load seems trivial. In addition to that, we’re happy to report that Watsco has boosted its EBIT by 50%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Watsco can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Watsco generated free cash flow amounting to a very robust 90% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

The good news is that Watsco’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! We think Watsco is no more beholden to its lenders, than the birds are to birdwatchers. For investing nerds like us its balance sheet is almost charming.