Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Frontdoor, Inc. (NASDAQ:FTDR) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Frontdoor Carry?

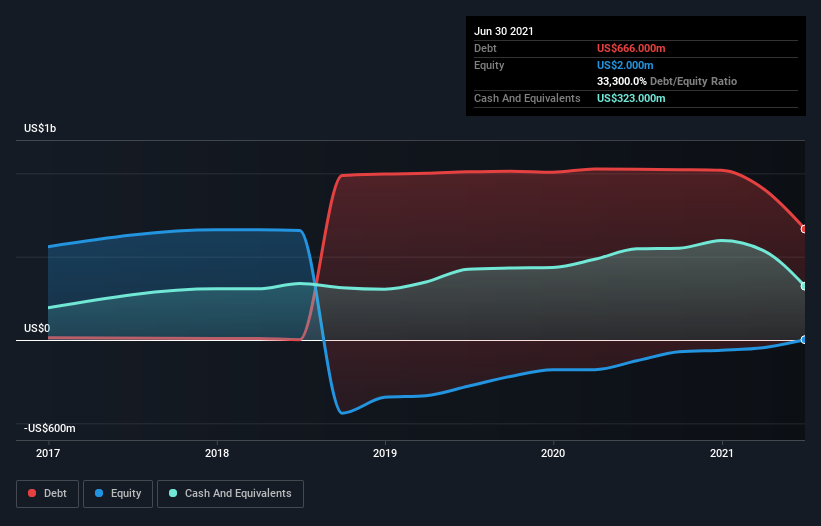

The image below, which you can click on for greater detail, shows that Frontdoor had debt of US$666.0m at the end of June 2021, a reduction from US$1.03b over a year. However, it also had US$323.0m in cash, and so its net debt is US$343.0m.

How Strong Is Frontdoor’s Balance Sheet?

According to the last reported balance sheet, Frontdoor had liabilities of US$423.0m due within 12 months, and liabilities of US$710.0m due beyond 12 months. Offsetting these obligations, it had cash of US$323.0m as well as receivables valued at US$9.00m due within 12 months. So it has liabilities totalling US$801.0m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Frontdoor has a market capitalization of US$3.56b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Looking at its net debt to EBITDA of 1.4 and interest cover of 4.1 times, it seems to us that Frontdoor is probably using debt in a pretty reasonable way. So we’d recommend keeping a close eye on the impact financing costs are having on the business. Unfortunately, Frontdoor’s EBIT flopped 15% over the last four quarters. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Frontdoor can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Frontdoor produced sturdy free cash flow equating to 72% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

When it comes to the balance sheet, the standout positive for Frontdoor was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren’t so heartening. In particular, EBIT growth rate gives us cold feet. When we consider all the factors mentioned above, we do feel a bit cautious about Frontdoor’s use of debt. While we appreciate debt can enhance returns on equity, we’d suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.