Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Verisk Analytics, Inc. (NASDAQ:VRSK) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Verisk Analytics’s Debt?

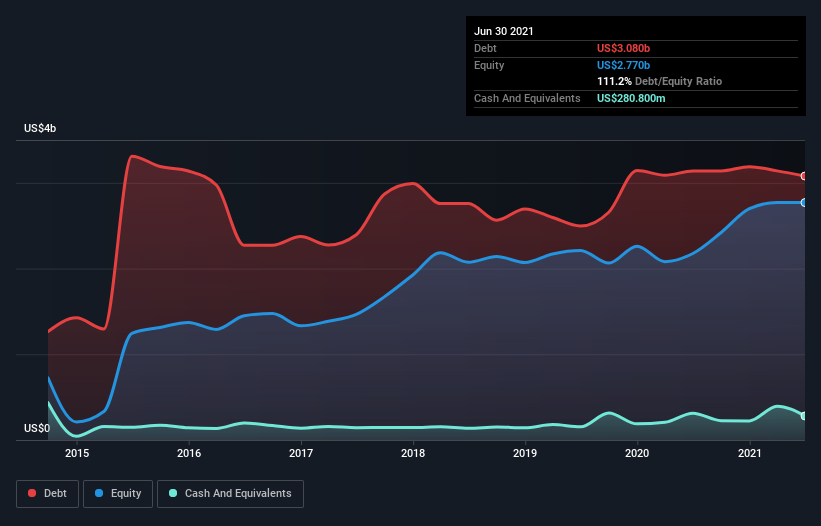

As you can see below, Verisk Analytics had US$3.08b of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$280.8m, its net debt is less, at about US$2.80b.

How Healthy Is Verisk Analytics’ Balance Sheet?

According to the last reported balance sheet, Verisk Analytics had liabilities of US$1.49b due within 12 months, and liabilities of US$3.45b due beyond 12 months. Offsetting these obligations, it had cash of US$280.8m as well as receivables valued at US$498.2m due within 12 months. So it has liabilities totalling US$4.16b more than its cash and near-term receivables, combined.

Since publicly traded Verisk Analytics shares are worth a very impressive total of US$31.4b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With a debt to EBITDA ratio of 2.1, Verisk Analytics uses debt artfully but responsibly. And the alluring interest cover (EBIT of 7.6 times interest expense) certainly does not do anything to dispel this impression. If Verisk Analytics can keep growing EBIT at last year’s rate of 16% over the last year, then it will find its debt load easier to manage. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Verisk Analytics can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Verisk Analytics generated free cash flow amounting to a very robust 85% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

Happily, Verisk Analytics’s impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And the good news does not stop there, as its EBIT growth rate also supports that impression! Zooming out, Verisk Analytics seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. When analysing debt levels, the balance sheet is the obvious place to start.