Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that DocuSign, Inc. (NASDAQ:DOCU) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does DocuSign Carry?

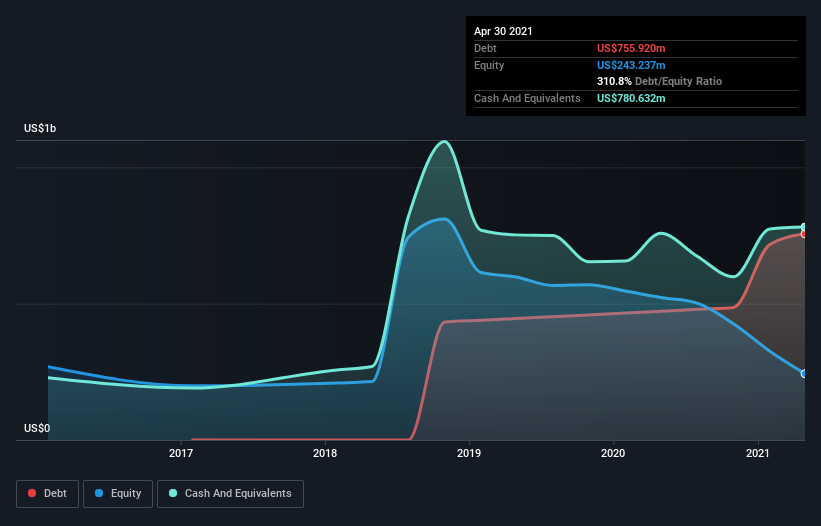

The image below, which you can click on for greater detail, shows that at April 2021 DocuSign had debt of US$755.9m, up from US$472.2m in one year. However, its balance sheet shows it holds US$780.6m in cash, so it actually has US$24.7m net cash.

How Healthy Is DocuSign’s Balance Sheet?

We can see from the most recent balance sheet that DocuSign had liabilities of US$1.10b falling due within a year, and liabilities of US$956.0m due beyond that. Offsetting these obligations, it had cash of US$780.6m as well as receivables valued at US$265.6m due within 12 months. So its liabilities total US$1.01b more than the combination of its cash and short-term receivables.

This state of affairs indicates that DocuSign’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it’s hard to imagine that the US$57.7b company is struggling for cash, we still think it’s worth monitoring its balance sheet. Despite its noteworthy liabilities, DocuSign boasts net cash, so it’s fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if DocuSign can strengthen its balance sheet over time.

Over 12 months, DocuSign reported revenue of US$1.6b, which is a gain of 54%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is DocuSign?

Although DocuSign had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$305m. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. The good news for DocuSign shareholders is that its revenue growth is strong, making it easier to raise capital if need be. But we still think it’s somewhat risky.