Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that PBF Energy Inc. (NYSE:PBF) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does PBF Energy Carry?

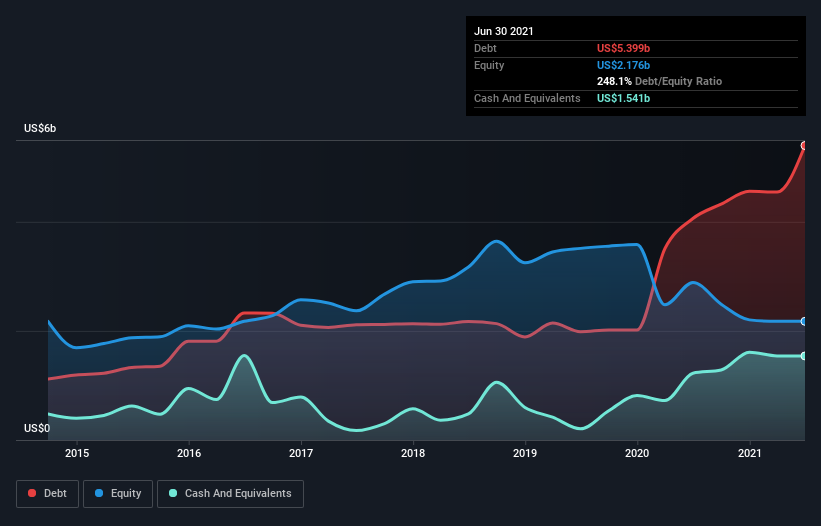

The image below, which you can click on for greater detail, shows that at March 2021 PBF Energy had debt of US$4.55b, up from US$4.06b in one year. On the flip side, it has US$1.54b in cash leading to net debt of about US$3.00b.

A Look At PBF Energy’s Liabilities

We can see from the most recent balance sheet that PBF Energy had liabilities of US$3.40b falling due within a year, and liabilities of US$5.69b due beyond that. Offsetting these obligations, it had cash of US$1.54b as well as receivables valued at US$861.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$6.69b.

This deficit casts a shadow over the US$1.10b company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. At the end of the day, PBF Energy would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if PBF Energy can strengthen its balance sheet over time.

In the last year PBF Energy had a loss before interest and tax, and actually shrunk its revenue by 6.7%, to US$19b. That’s not what we would hope to see.

Caveat Emptor

Importantly, PBF Energy had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping US$1.3b. Reflecting on this and the significant total liabilities, it’s hard to know what to say about the stock because of our intense dis-affinity for it. Like every long-shot we’re sure it has a glossy presentation outlining its blue-sky potential. But the reality is that it is low on liquid assets relative to liabilities, and it lost US$709m in the last year. So we think buying this stock is risky.