Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that EQT Corporation (NYSE:EQT) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does EQT Carry?

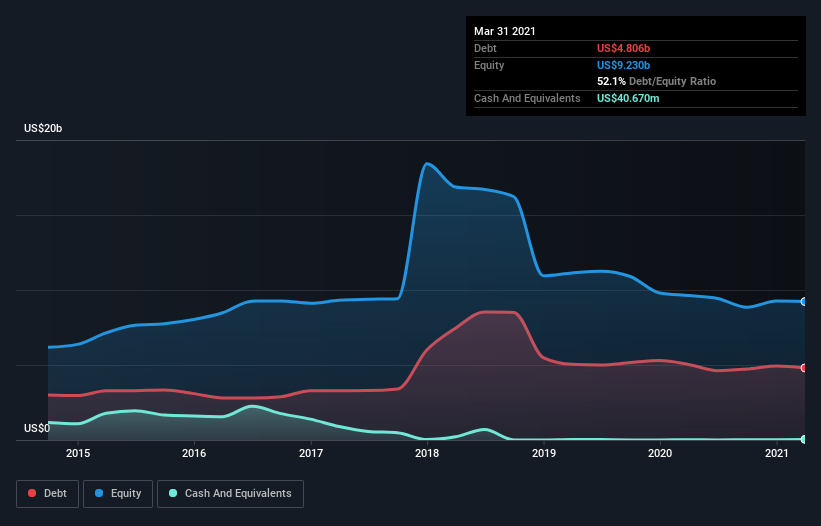

As you can see below, EQT had US$4.76b of debt at March 2021, down from US$5.04b a year prior. Net debt is about the same, since the it doesn’t have much cash.

How Strong Is EQT’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that EQT had liabilities of US$1.75b due within 12 months and liabilities of US$7.06b due beyond that. On the other hand, it had cash of US$40.7m and US$682.5m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$8.09b.

Given this deficit is actually higher than the company’s market capitalization of US$7.64b, we think shareholders really should watch EQT’s debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine EQT’s ability to maintain a healthy balance sheet going forward.

Over 12 months, EQT made a loss at the EBIT level, and saw its revenue drop to US$3.0b, which is a fall of 4.9%. That’s not what we would hope to see.

Caveat Emptor

Importantly, EQT had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at US$620m. When we look at that alongside the significant liabilities, we’re not particularly confident about the company. We’d want to see some strong near-term improvements before getting too interested in the stock. It’s fair to say the loss of US$841m didn’t encourage us either; we’d like to see a profit. In the meantime, we consider the stock to be risky. When analysing debt levels, the balance sheet is the obvious place to start.