Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Beasley Broadcast Group, Inc. (NASDAQ:BBGI) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Beasley Broadcast Group Carry?

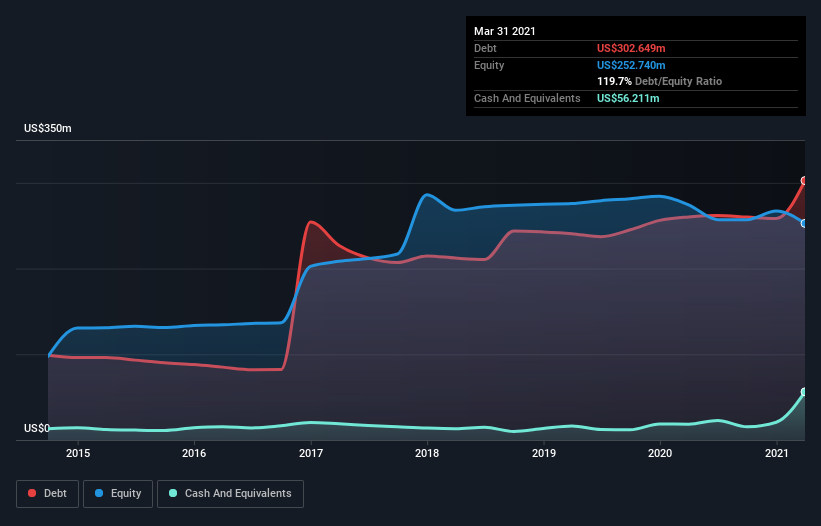

As you can see below, at the end of March 2021, Beasley Broadcast Group had US$302.6m of debt, up from US$260.2m a year ago. Click the image for more detail. However, because it has a cash reserve of US$56.2m, its net debt is less, at about US$246.4m.

How Healthy Is Beasley Broadcast Group’s Balance Sheet?

The latest balance sheet data shows that Beasley Broadcast Group had liabilities of US$37.6m due within a year, and liabilities of US$471.7m falling due after that. On the other hand, it had cash of US$56.2m and US$36.7m worth of receivables due within a year. So it has liabilities totalling US$416.5m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$95.0m company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. After all, Beasley Broadcast Group would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Beasley Broadcast Group’s ability to maintain a healthy balance sheet going forward.

In the last year Beasley Broadcast Group had a loss before interest and tax, and actually shrunk its revenue by 25%, to US$197m. That makes us nervous, to say the least.

Caveat Emptor

While Beasley Broadcast Group’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost US$2.1m at the EBIT level. If you consider the significant liabilities mentioned above, we are extremely wary of this investment. Of course, it may be able to improve its situation with a bit of luck and good execution. But we think that is unlikely, given it is low on liquid assets, and burned through US$448k in the last year. So we think this stock is risky, like walking through a dirty dog park with a mask on. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.