Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Zynga Inc. (NASDAQ:ZNGA) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Zynga Carry?

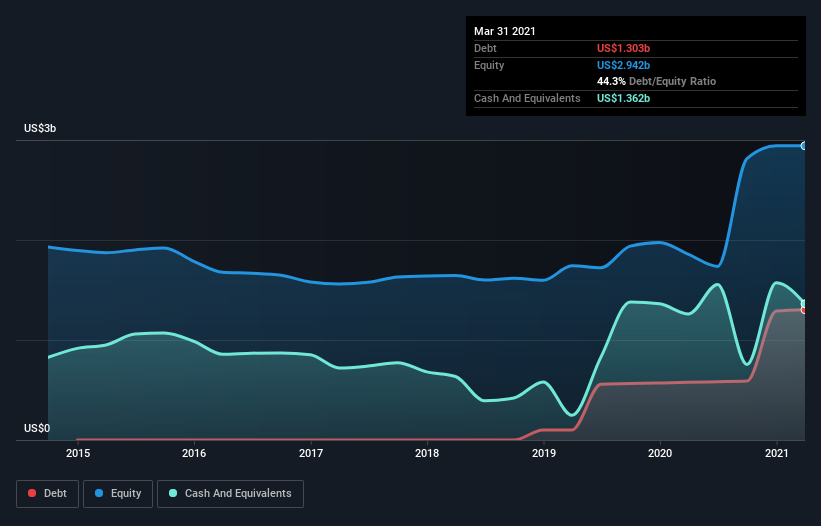

As you can see below, at the end of March 2021, Zynga had US$1.30b of debt, up from US$576.7m a year ago. Click the image for more detail. However, its balance sheet shows it holds US$1.36b in cash, so it actually has US$58.6m net cash.

How Healthy Is Zynga’s Balance Sheet?

We can see from the most recent balance sheet that Zynga had liabilities of US$1.42b falling due within a year, and liabilities of US$1.64b due beyond that. Offsetting these obligations, it had cash of US$1.36b as well as receivables valued at US$274.6m due within 12 months. So it has liabilities totalling US$1.43b more than its cash and near-term receivables, combined.

Of course, Zynga has a titanic market capitalization of US$11.9b, so these liabilities are probably manageable. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, Zynga boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Zynga’s ability to maintain a healthy balance sheet going forward.

In the last year Zynga wasn’t profitable at an EBIT level, but managed to grow its revenue by 54%, to US$2.3b. With any luck the company will be able to grow its way to profitability.

So How Risky Is Zynga?

Although Zynga had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$282m. So taking that on face value, and considering the net cash situation, we don’t think that the stock is too risky in the near term. The good news for Zynga shareholders is that its revenue growth is strong, making it easier to raise capital if need be. But we still think it’s somewhat risky. When analysing debt levels, the balance sheet is the obvious place to start.