Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, AngioDynamics, Inc. (NASDAQ:ANGO) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does AngioDynamics Carry?

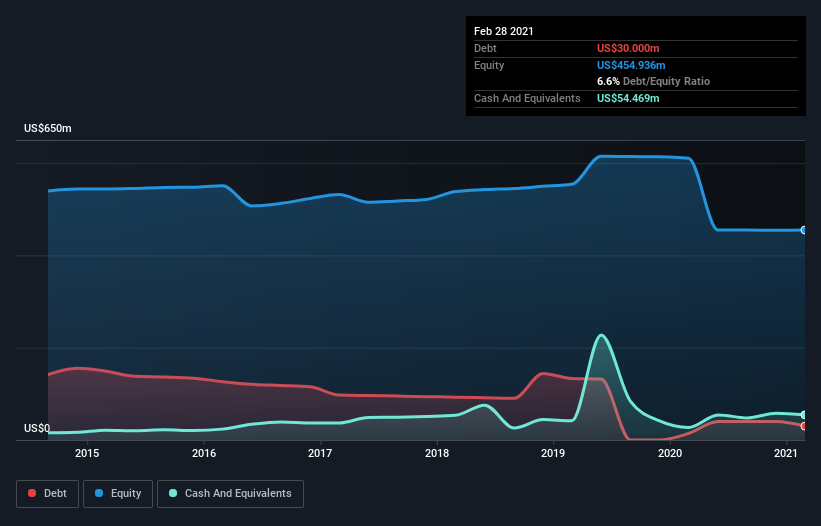

The image below, which you can click on for greater detail, shows that at February 2021 AngioDynamics had debt of US$30.0m, up from US$14.3m in one year. However, its balance sheet shows it holds US$54.5m in cash, so it actually has US$24.5m net cash.

How Strong Is AngioDynamics’ Balance Sheet?

The latest balance sheet data shows that AngioDynamics had liabilities of US$50.3m due within a year, and liabilities of US$77.1m falling due after that. On the other hand, it had cash of US$54.5m and US$33.2m worth of receivables due within a year. So its liabilities total US$39.7m more than the combination of its cash and short-term receivables.

Given AngioDynamics has a market capitalization of US$876.8m, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, AngioDynamics also has more cash than debt, so we’re pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine AngioDynamics’s ability to maintain a healthy balance sheet going forward.

In the last year AngioDynamics’s revenue was pretty flat, and it made a negative EBIT. While that’s not too bad, we’d prefer see growth.

So How Risky Is AngioDynamics?

Although AngioDynamics had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$9.7m. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. Until we see some positive EBIT, we’re a bit cautious of the stock, not least because of the rather modest revenue growth. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.