Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Cardinal Health, Inc. (NYSE:CAH) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

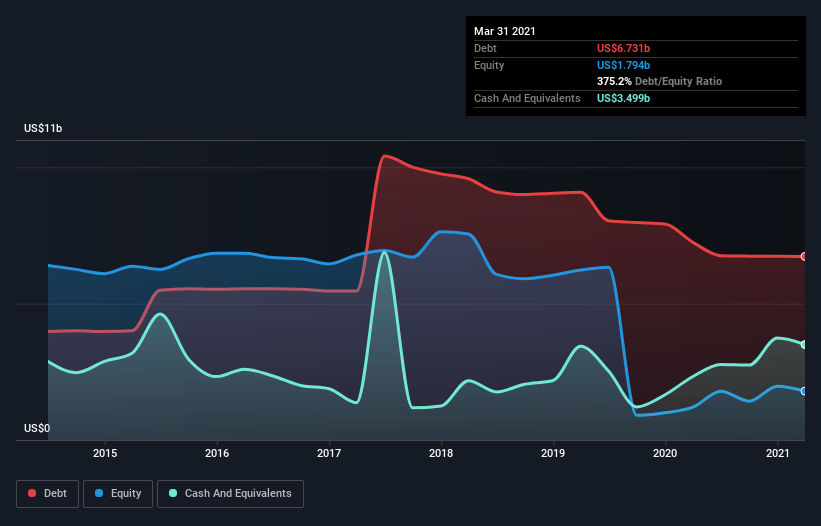

What Is Cardinal Health’s Net Debt?

As you can see below, Cardinal Health had US$6.25b of debt at March 2021, down from US$7.25b a year prior. However, it also had US$3.50b in cash, and so its net debt is US$2.75b.

A Look At Cardinal Health’s Liabilities

We can see from the most recent balance sheet that Cardinal Health had liabilities of US$25.3b falling due within a year, and liabilities of US$16.8b due beyond that. Offsetting this, it had US$3.50b in cash and US$8.73b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$29.9b.

The deficiency here weighs heavily on the US$16.3b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, Cardinal Health would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Cardinal Health’s net debt is only 1.0 times its EBITDA. And its EBIT easily covers its interest expense, being 10.2 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. The good news is that Cardinal Health has increased its EBIT by 3.7% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Cardinal Health’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Cardinal Health actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Neither Cardinal Health’s ability to handle its total liabilities nor its EBIT growth rate gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. We should also note that Healthcare industry companies like Cardinal Health commonly do use debt without problems. We think that Cardinal Health’s debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.