The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Aura Minerals Inc. (TSE:ORA) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Aura Minerals Carry?

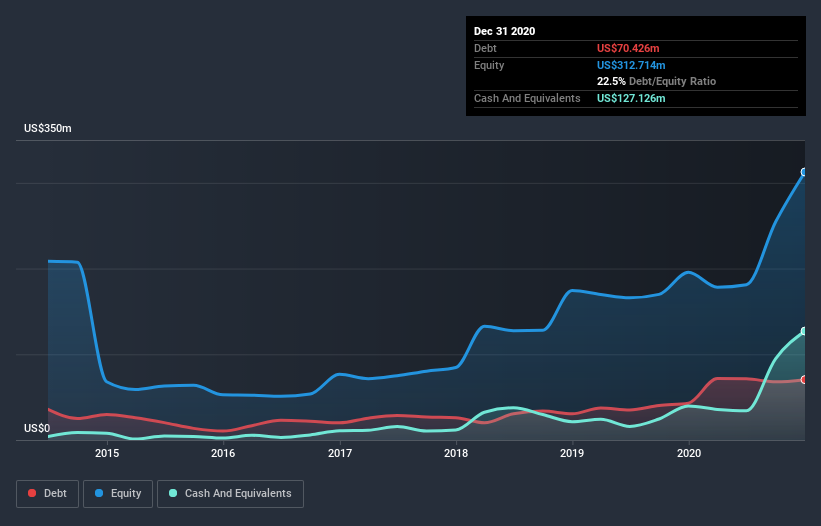

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Aura Minerals had US$70.4m of debt, an increase on US$43.0m, over one year. However, it does have US$127.1m in cash offsetting this, leading to net cash of US$56.7m.

How Strong Is Aura Minerals’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Aura Minerals had liabilities of US$120.7m due within 12 months and liabilities of US$102.8m due beyond that. On the other hand, it had cash of US$127.1m and US$35.8m worth of receivables due within a year. So its liabilities total US$60.6m more than the combination of its cash and short-term receivables.

Of course, Aura Minerals has a market capitalization of US$751.0m, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Aura Minerals boasts net cash, so it’s fair to say it does not have a heavy debt load!

Even more impressive was the fact that Aura Minerals grew its EBIT by 237% over twelve months. That boost will make it even easier to pay down debt going forward. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Aura Minerals can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Aura Minerals may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Aura Minerals reported free cash flow worth 19% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Summing up

We could understand if investors are concerned about Aura Minerals’s liabilities, but we can be reassured by the fact it has has net cash of US$56.7m. And it impressed us with its EBIT growth of 237% over the last year. So we don’t think Aura Minerals’s use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.