Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Shift4 Payments, Inc. (NYSE:FOUR) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Shift4 Payments Carry?

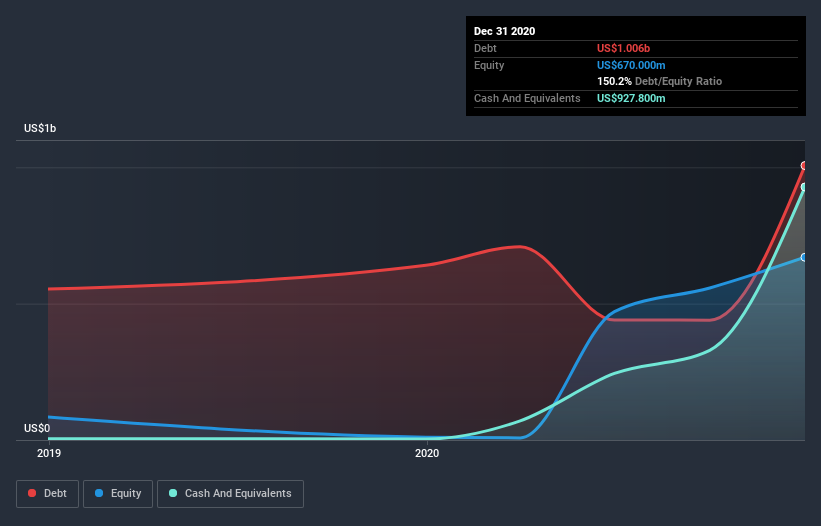

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Shift4 Payments had US$1.01b of debt, an increase on US$640.4m, over one year. However, it does have US$927.8m in cash offsetting this, leading to net debt of about US$78.5m.

How Healthy Is Shift4 Payments’ Balance Sheet?

We can see from the most recent balance sheet that Shift4 Payments had liabilities of US$99.4m falling due within a year, and liabilities of US$1.01b due beyond that. Offsetting these obligations, it had cash of US$927.8m as well as receivables valued at US$94.2m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$87.3m.

This state of affairs indicates that Shift4 Payments’ balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it’s hard to imagine that the US$7.96b company is struggling for cash, we still think it’s worth monitoring its balance sheet. Carrying virtually no net debt, Shift4 Payments has a very light debt load indeed. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Shift4 Payments’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Shift4 Payments reported revenue of US$767m, which is a gain of 4.8%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Shift4 Payments had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at US$67m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled US$29m in negative free cash flow over the last twelve months. So to be blunt we think it is risky. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.