Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Curtiss-Wright Corporation (NYSE:CW) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Curtiss-Wright’s Net Debt?

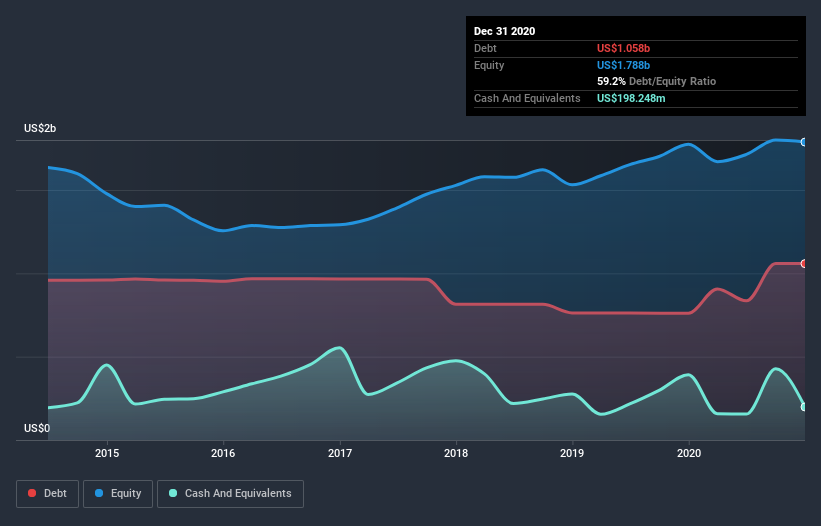

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Curtiss-Wright had US$1.06b of debt, an increase on US$760.6m, over one year. However, because it has a cash reserve of US$198.2m, its net debt is less, at about US$860.0m.

How Healthy Is Curtiss-Wright’s Balance Sheet?

The latest balance sheet data shows that Curtiss-Wright had liabilities of US$810.4m due within a year, and liabilities of US$1.42b falling due after that. Offsetting this, it had US$198.2m in cash and US$588.7m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.45b.

While this might seem like a lot, it is not so bad since Curtiss-Wright has a market capitalization of US$5.17b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

We’d say that Curtiss-Wright’s moderate net debt to EBITDA ratio ( being 1.7), indicates prudence when it comes to debt. And its strong interest cover of 10.8 times, makes us even more comfortable. Sadly, Curtiss-Wright’s EBIT actually dropped 9.8% in the last year. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Curtiss-Wright’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Curtiss-Wright recorded free cash flow worth 71% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Curtiss-Wright’s interest cover was a real positive on this analysis, as was its conversion of EBIT to free cash flow. On the other hand, its EBIT growth rate makes us a little less comfortable about its debt. Considering this range of data points, we think Curtiss-Wright is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.