David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Sempra (NYSE:SRE) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Sempra’s Debt?

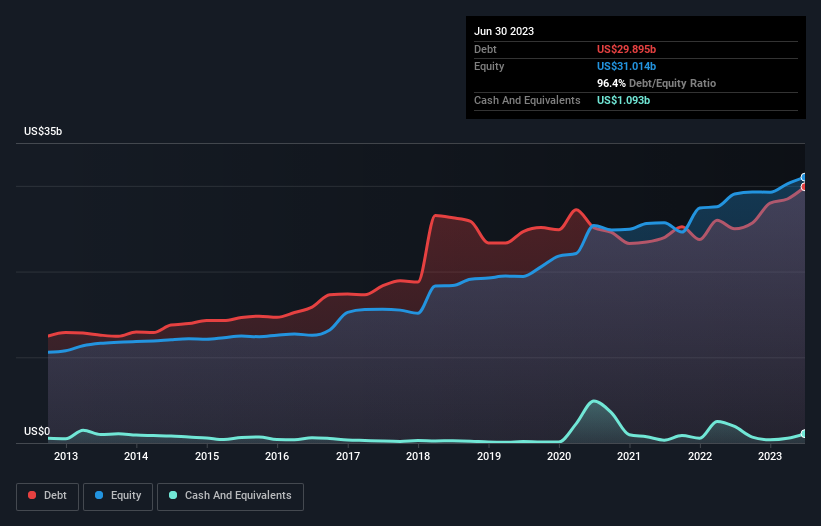

As you can see below, at the end of June 2023, Sempra had US$29.9b of debt, up from US$25.0b a year ago. Click the image for more detail. However, it does have US$1.09b in cash offsetting this, leading to net debt of about US$28.8b.

How Healthy Is Sempra’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Sempra had liabilities of US$8.45b due within 12 months and liabilities of US$43.3b due beyond that. Offsetting these obligations, it had cash of US$1.09b as well as receivables valued at US$2.54b due within 12 months. So its liabilities total US$48.1b more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company’s massive market capitalization of US$46.3b, we think shareholders really should watch Sempra’s debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Sempra has a rather high debt to EBITDA ratio of 5.4 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 3.0 times, suggesting it can responsibly service its obligations. Fortunately, Sempra grew its EBIT by 8.7% in the last year, slowly shrinking its debt relative to earnings. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Sempra’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Sempra saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Sempra’s net debt to EBITDA left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. We should also note that Integrated Utilities industry companies like Sempra commonly do use debt without problems. Overall, it seems to us that Sempra’s balance sheet is really quite a risk to the business. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they say. There’s no doubt that we learn most about debt from the balance sheet.