Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Tennant Company (NYSE:TNC) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Tennant Carry?

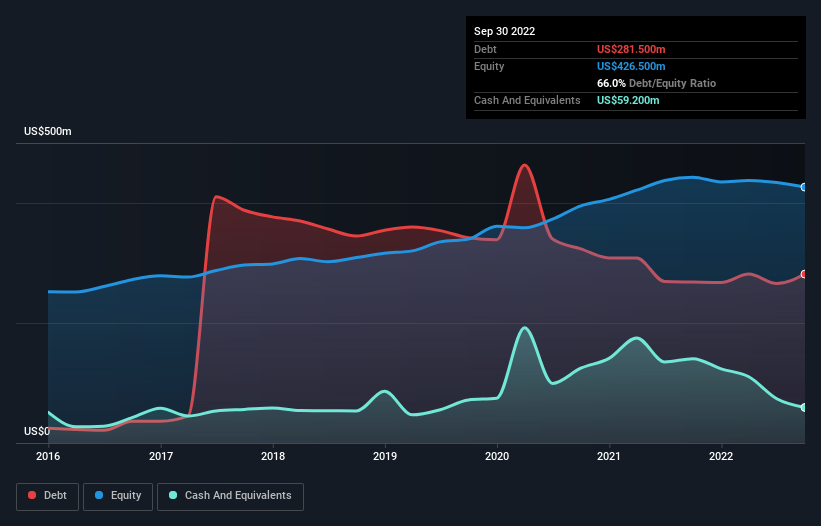

As you can see below, at the end of September 2022, Tennant had US$281.5m of debt, up from US$268.3m a year ago. Click the image for more detail. On the flip side, it has US$59.2m in cash leading to net debt of about US$222.3m.

How Healthy Is Tennant’s Balance Sheet?

We can see from the most recent balance sheet that Tennant had liabilities of US$244.2m falling due within a year, and liabilities of US$334.4m due beyond that. Offsetting these obligations, it had cash of US$59.2m as well as receivables valued at US$219.3m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$300.1m.

This deficit isn’t so bad because Tennant is worth US$1.19b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

We’d say that Tennant’s moderate net debt to EBITDA ratio ( being 1.8), indicates prudence when it comes to debt. And its strong interest cover of 16.5 times, makes us even more comfortable. The bad news is that Tennant saw its EBIT decline by 13% over the last year. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Tennant can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Tennant’s free cash flow amounted to 42% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Tennant’s EBIT growth rate and conversion of EBIT to free cash flow definitely weigh on it, in our esteem. But the good news is it seems to be able to cover its interest expense with its EBIT with ease. We think that Tennant’s debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There’s no doubt that we learn most about debt from the balance sheet.