Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Charge Enterprises, Inc. (NASDAQ:CRGE) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Charge Enterprises’s Debt?

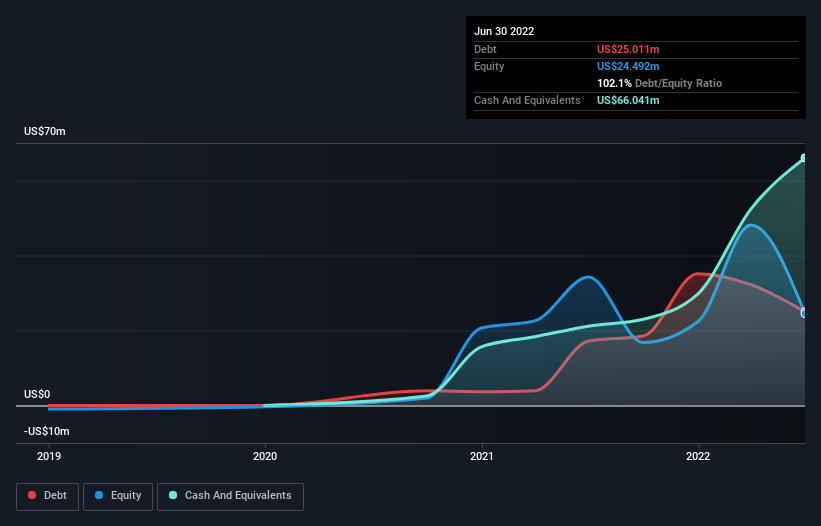

The image below, which you can click on for greater detail, shows that at June 2022 Charge Enterprises had debt of US$25.0m, up from US$17.2m in one year. But on the other hand it also has US$66.0m in cash, leading to a US$41.0m net cash position.

How Strong Is Charge Enterprises’ Balance Sheet?

According to the last reported balance sheet, Charge Enterprises had liabilities of US$157.9m due within 12 months, and liabilities of US$24.9m due beyond 12 months. On the other hand, it had cash of US$66.0m and US$83.3m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$33.4m.

Given Charge Enterprises has a market capitalization of US$684.4m, it’s hard to believe these liabilities pose much threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Charge Enterprises also has more cash than debt, so we’re pretty confident it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Charge Enterprises can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Charge Enterprises reported revenue of US$580m, which is a gain of 78%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is Charge Enterprises?

While Charge Enterprises lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow US$11m. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. The good news for Charge Enterprises shareholders is that its revenue growth is strong, making it easier to raise capital if need be. But that doesn’t change our opinion that the stock is risky. The balance sheet is clearly the area to focus on when you are analysing debt.