Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that SeaSpine Holdings Corporation (NASDAQ:SPNE) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is SeaSpine Holdings’s Net Debt?

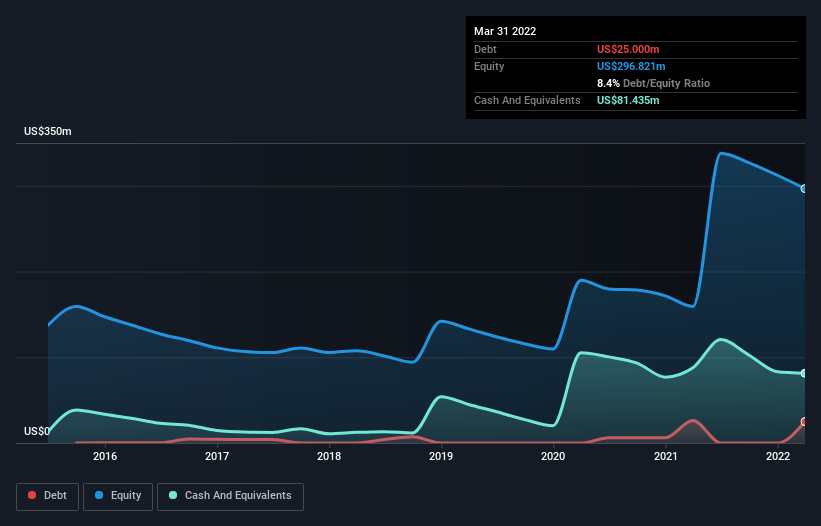

The image below, which you can click on for greater detail, shows that SeaSpine Holdings had debt of US$25.0m at the end of March 2022, a reduction from US$26.2m over a year. However, it does have US$81.4m in cash offsetting this, leading to net cash of US$56.4m.

A Look At SeaSpine Holdings’ Liabilities

Zooming in on the latest balance sheet data, we can see that SeaSpine Holdings had liabilities of US$73.0m due within 12 months and liabilities of US$10.6m due beyond that. Offsetting this, it had US$81.4m in cash and US$36.1m in receivables that were due within 12 months. So it can boast US$33.9m more liquid assets than total liabilities.

This short term liquidity is a sign that SeaSpine Holdings could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, SeaSpine Holdings boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if SeaSpine Holdings can strengthen its balance sheet over time.

Over 12 months, SeaSpine Holdings reported revenue of US$200m, which is a gain of 25%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is SeaSpine Holdings?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months SeaSpine Holdings lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$79m of cash and made a loss of US$58m. But the saving grace is the US$56.4m on the balance sheet. That means it could keep spending at its current rate for more than two years. SeaSpine Holdings’s revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start.