Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Ciena Corporation (NYSE:CIEN) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Ciena Carry?

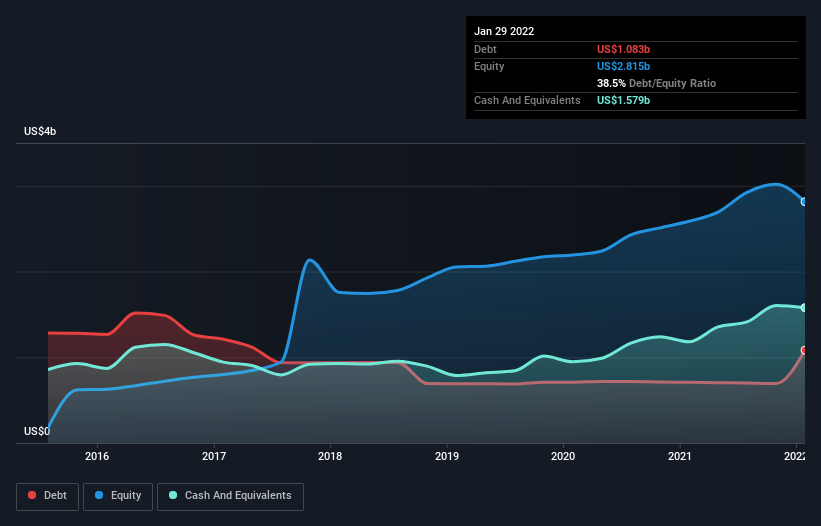

You can click the graphic below for the historical numbers, but it shows that as of January 2022 Ciena had US$1.08b of debt, an increase on US$708.0m, over one year. But on the other hand it also has US$1.58b in cash, leading to a US$496.0m net cash position.

How Strong Is Ciena’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Ciena had liabilities of US$760.3m due within 12 months and liabilities of US$1.33b due beyond that. Offsetting these obligations, it had cash of US$1.58b as well as receivables valued at US$924.2m due within 12 months. So it actually has US$417.6m more liquid assets than total liabilities.

This surplus suggests that Ciena has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Ciena boasts net cash, so it’s fair to say it does not have a heavy debt load!

But the other side of the story is that Ciena saw its EBIT decline by 8.5% over the last year. If earnings continue to decline at that rate the company may have increasing difficulty managing its debt load. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Ciena can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Ciena may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Ciena generated free cash flow amounting to a very robust 85% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Summing up

While it is always sensible to investigate a company’s debt, in this case Ciena has US$496.0m in net cash and a decent-looking balance sheet. The cherry on top was that in converted 85% of that EBIT to free cash flow, bringing in US$410m. So is Ciena’s debt a risk? It doesn’t seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt.