Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Zscaler, Inc. (NASDAQ:ZS) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Zscaler’s Net Debt?

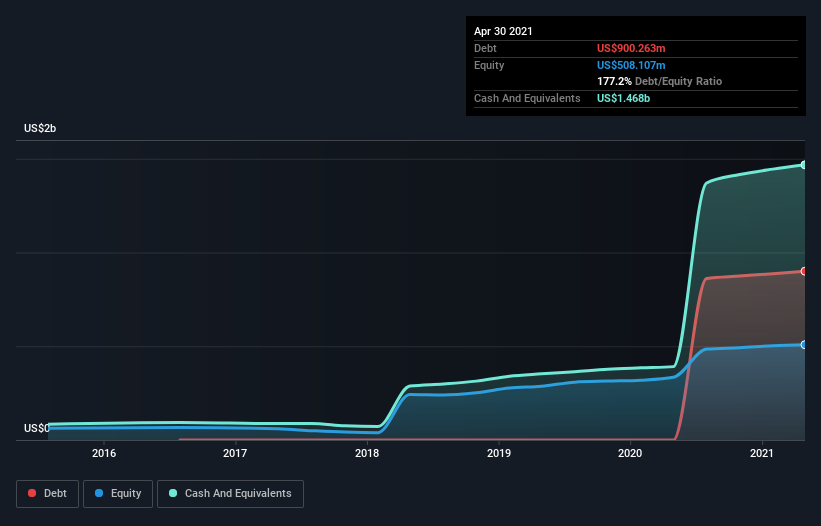

You can click the graphic below for the historical numbers, but it shows that as of April 2021 Zscaler had US$900.3m of debt, an increase on none, over one year. But on the other hand it also has US$1.47b in cash, leading to a US$567.3m net cash position.

How Strong Is Zscaler’s Balance Sheet?

We can see from the most recent balance sheet that Zscaler had liabilities of US$564.9m falling due within a year, and liabilities of US$989.3m due beyond that. On the other hand, it had cash of US$1.47b and US$168.6m worth of receivables due within a year. So it actually has US$82.1m more liquid assets than total liabilities.

This state of affairs indicates that Zscaler’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it’s very unlikely that the US$33.5b company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, Zscaler boasts net cash, so it’s fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Zscaler’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Zscaler reported revenue of US$602m, which is a gain of 54%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is Zscaler?

Although Zscaler had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$127m. So taking that on face value, and considering the net cash situation, we don’t think that the stock is too risky in the near term. Keeping in mind its 54% revenue growth over the last year, we think there’s a decent chance the company is on track. We’d see further strong growth as an optimistic indication.