Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Marvell Technology, Inc. (NASDAQ:MRVL) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Marvell Technology Carry?

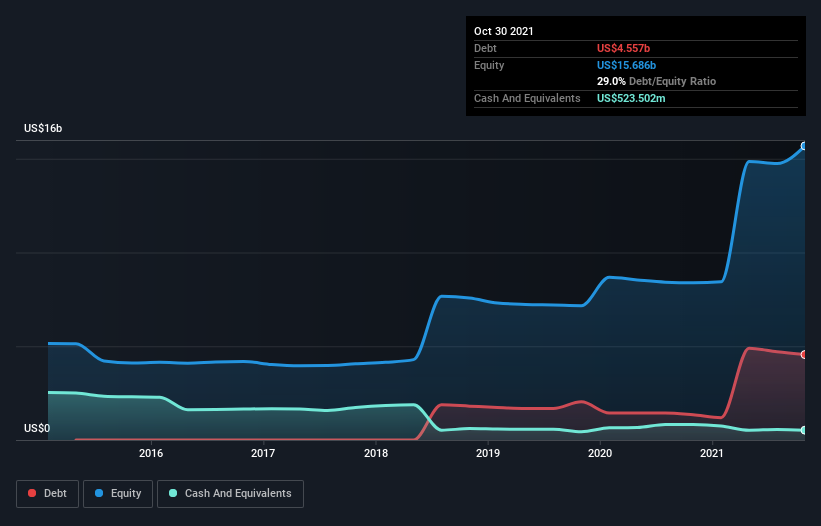

The image below, which you can click on for greater detail, shows that at October 2021 Marvell Technology had debt of US$4.56b, up from US$1.34b in one year. However, it also had US$523.5m in cash, and so its net debt is US$4.03b.

How Healthy Is Marvell Technology’s Balance Sheet?

According to the last reported balance sheet, Marvell Technology had liabilities of US$1.24b due within 12 months, and liabilities of US$5.09b due beyond 12 months. Offsetting these obligations, it had cash of US$523.5m as well as receivables valued at US$978.3m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.83b.

Given Marvell Technology has a humongous market capitalization of US$70.1b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Marvell Technology’s ability to maintain a healthy balance sheet going forward.

In the last year Marvell Technology wasn’t profitable at an EBIT level, but managed to grow its revenue by 36%, to US$3.9b. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

While we can certainly appreciate Marvell Technology’s revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. To be specific the EBIT loss came in at US$54m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. For example, we would not want to see a repeat of last year’s loss of US$411m. So we do think this stock is quite risky.