Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Willamette Valley Vineyards, Inc. (NASDAQ:WVVI) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Willamette Valley Vineyards’s Debt?

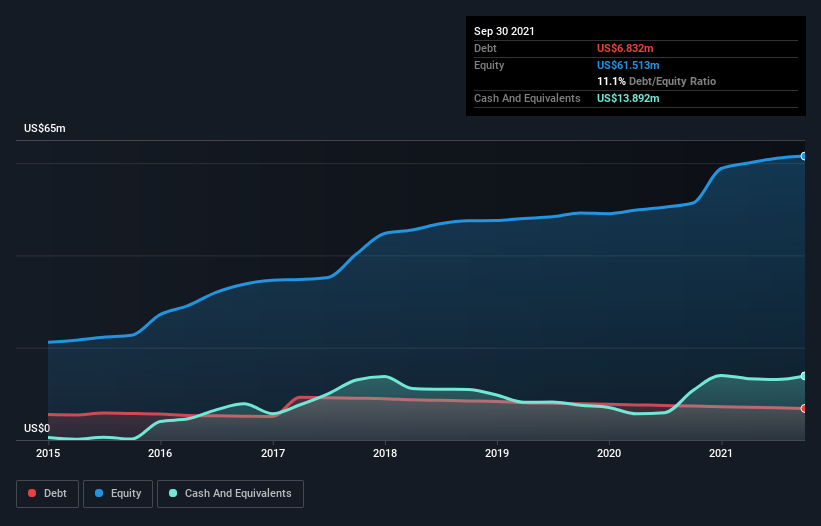

The image below, which you can click on for greater detail, shows that Willamette Valley Vineyards had debt of US$6.83m at the end of September 2021, a reduction from US$7.35m over a year. However, its balance sheet shows it holds US$13.9m in cash, so it actually has US$7.06m net cash.

A Look At Willamette Valley Vineyards’ Liabilities

According to the last reported balance sheet, Willamette Valley Vineyards had liabilities of US$10.7m due within 12 months, and liabilities of US$12.6m due beyond 12 months. Offsetting this, it had US$13.9m in cash and US$2.36m in receivables that were due within 12 months. So its liabilities total US$7.02m more than the combination of its cash and short-term receivables.

Since publicly traded Willamette Valley Vineyards shares are worth a total of US$66.0m, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Willamette Valley Vineyards also has more cash than debt, so we’re pretty confident it can manage its debt safely.

But the bad news is that Willamette Valley Vineyards has seen its EBIT plunge 12% in the last twelve months. If that rate of decline in earnings continues, the company could find itself in a tight spot. There’s no doubt that we learn most about debt from the balance sheet. But you can’t view debt in total isolation; since Willamette Valley Vineyards will need earnings to service that debt. So when considering debt, it’s definitely worth looking at the earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Willamette Valley Vineyards may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Willamette Valley Vineyards burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Summing up

Although Willamette Valley Vineyards’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$7.06m. So while Willamette Valley Vineyards does not have a great balance sheet, it’s certainly not too bad. The balance sheet is clearly the area to focus on when you are analysing debt.