Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. This article will consider whether Boeing‘s (NYSE:BA) statutory profits are a good guide to its underlying earnings.

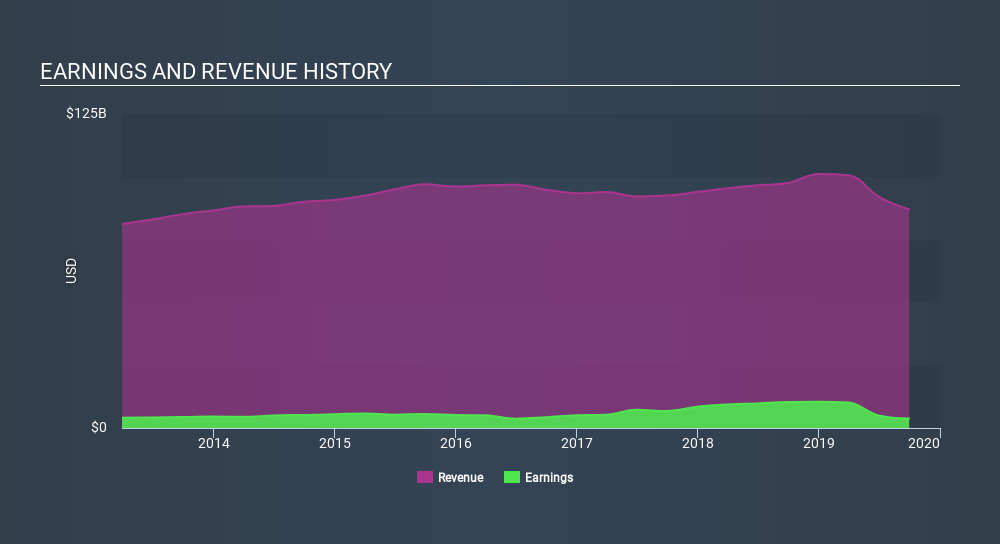

We like the fact that Boeing made a profit of US$3.80b on its revenue of US$87.0b, in the last year. Below, you can see that both its revenue and its profit have fallen over the last three years.

Not all profits are equal, and we can learn more about the nature of a company’s past profitability by diving deeper into the financial statements. So today we’ll look at what Boeing’s cashflow tells us about the quality of its earnings. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

A Closer Look At Boeing’s Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company’s profit exceeds its FCF.

Therefore, it’s actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it’s worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Over the twelve months to September 2019, Boeing recorded an accrual ratio of 0.56. Ergo, its free cash flow is significantly weaker than its profit. Statistically speaking, that’s a real negative for future earnings. To wit, it produced free cash flow of US$806m during the period, falling well short of its reported profit of US$3.80b. Boeing’s free cash flow actually declined over the last year, but it may bounce back next year, since free cash flow is often more volatile than accounting profits.

One positive for Boeing shareholders is that it’s accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Our Take On Boeing’s Profit Performance

As we have made quite clear, we’re a bit worried that Boeing didn’t back up the last year’s profit with free cashflow. As a result, we think it may well be the case that Boeing’s underlying earnings power is lower than its statutory profit. In further bad news, its earnings per share decreased in the last year. At the end of the day, it’s essential to consider more than just the factors above, if you want to understand the company properly. Obviously, we love to consider the historical data to inform our opinion of a company. But it can be really valuable to consider what other analysts are forecasting. So feel free to check out our free graph representing analyst forecasts.

Today we’ve zoomed in on a single data point to better understand the nature of Boeing’s profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.