David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Warner Music Group Corp. (NASDAQ:WMG) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Warner Music Group’s Debt?

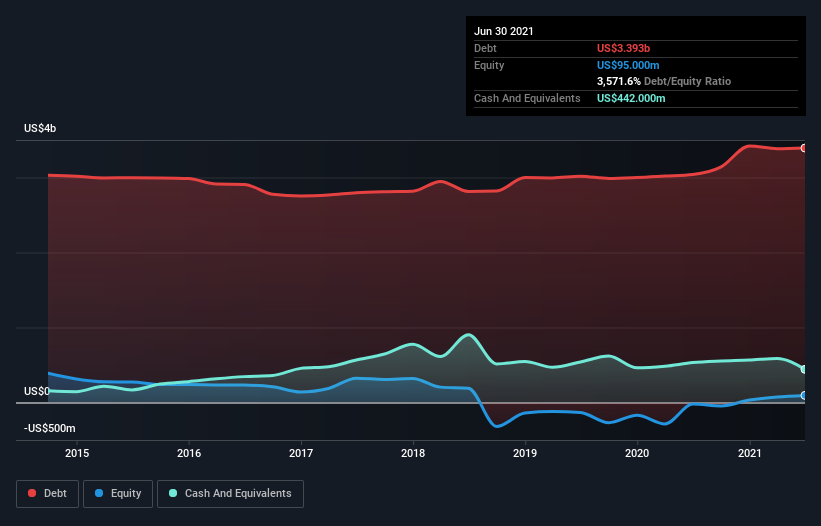

You can click the graphic below for the historical numbers, but it shows that as of June 2021 Warner Music Group had US$3.39b of debt, an increase on US$3.04b, over one year. However, it does have US$442.0m in cash offsetting this, leading to net debt of about US$2.95b.

How Strong Is Warner Music Group’s Balance Sheet?

According to the last reported balance sheet, Warner Music Group had liabilities of US$2.90b due within 12 months, and liabilities of US$4.04b due beyond 12 months. On the other hand, it had cash of US$442.0m and US$834.0m worth of receivables due within a year. So it has liabilities totalling US$5.67b more than its cash and near-term receivables, combined.

Warner Music Group has a very large market capitalization of US$19.6b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Warner Music Group’s debt is 2.9 times its EBITDA, and its EBIT cover its interest expense 5.9 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. We also note that Warner Music Group improved its EBIT from a last year’s loss to a positive US$720m. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Warner Music Group’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. In the last year, Warner Music Group created free cash flow amounting to 2.8% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

Warner Music Group’s conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to to cover its interest expense with its EBIT isn’t too shabby at all. Taking the abovementioned factors together we do think Warner Music Group’s debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. There’s no doubt that we learn most about debt from the balance sheet.