David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Unitil Corporation (NYSE:UTL) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Unitil’s Debt?

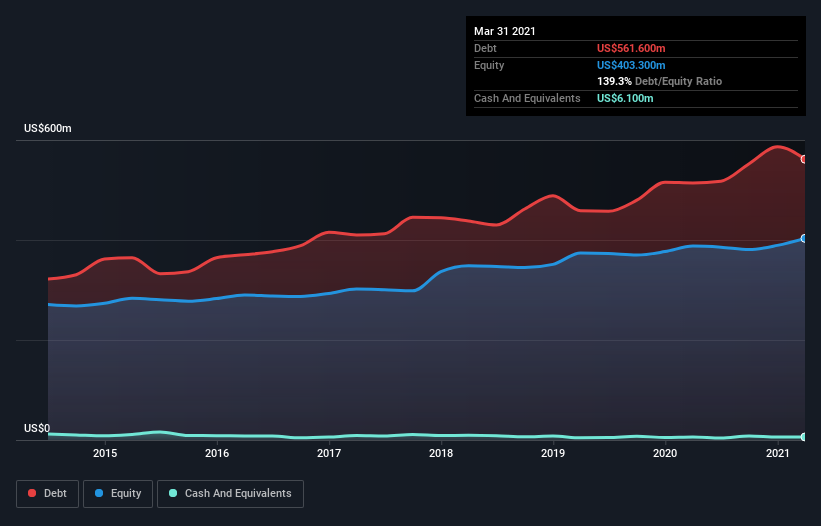

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Unitil had US$561.6m of debt, an increase on US$514.2m, over one year. And it doesn’t have much cash, so its net debt is about the same.

How Strong Is Unitil’s Balance Sheet?

The latest balance sheet data shows that Unitil had liabilities of US$122.9m due within a year, and liabilities of US$950.8m falling due after that. Offsetting these obligations, it had cash of US$6.10m as well as receivables valued at US$83.9m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$983.7m.

Given this deficit is actually higher than the company’s market capitalization of US$853.5m, we think shareholders really should watch Unitil’s debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Unitil has a low net debt to EBITDA ratio of only 1.4. And its EBIT covers its interest expense a whopping 12.9 times over. So we’re pretty relaxed about its super-conservative use of debt. Better yet, Unitil grew its EBIT by 230% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Unitil’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Considering the last two years, Unitil actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

While Unitil’s conversion of EBIT to free cash flow has us nervous. For example, its interest cover and EBIT growth rate give us some confidence in its ability to manage its debt. We should also note that Integrated Utilities industry companies like Unitil commonly do use debt without problems. We think that Unitil’s debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.