Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Target Corporation (NYSE:TGT) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Target’s Debt?

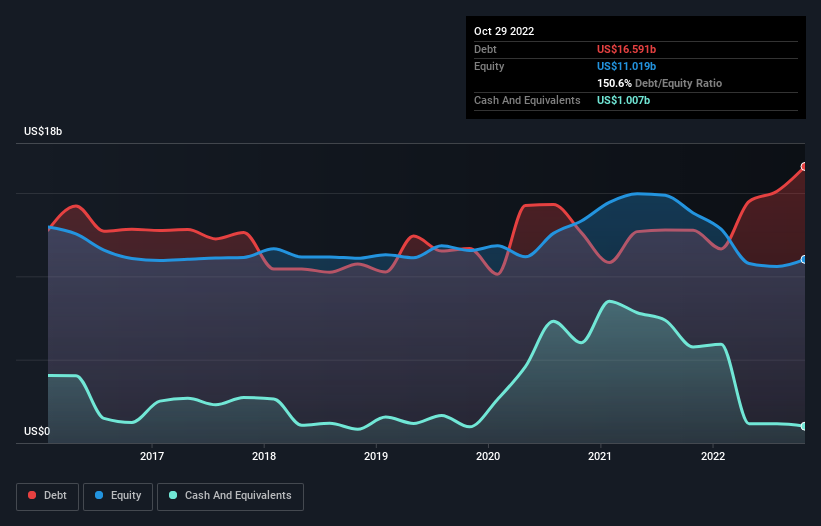

You can click the graphic below for the historical numbers, but it shows that as of October 2022 Target had US$16.6b of debt, an increase on US$12.8b, over one year. However, it also had US$1.01b in cash, and so its net debt is US$15.6b.

How Strong Is Target’s Balance Sheet?

We can see from the most recent balance sheet that Target had liabilities of US$23.8b falling due within a year, and liabilities of US$20.8b due beyond that. Offsetting this, it had US$1.01b in cash and US$1.35b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$42.2b.

This deficit is considerable relative to its very significant market capitalization of US$65.9b, so it does suggest shareholders should keep an eye on Target’s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Target’s net debt to EBITDA ratio of about 2.1 suggests only moderate use of debt. And its commanding EBIT of 10.8 times its interest expense, implies the debt load is as light as a peacock feather. Importantly, Target’s EBIT fell a jaw-dropping 45% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Target can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Target produced sturdy free cash flow equating to 58% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Target’s EBIT growth rate was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example its interest cover was refreshing. When we consider all the factors discussed, it seems to us that Target is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. The balance sheet is clearly the area to focus on when you are analysing debt.