David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Open Text Corporation (NASDAQ:OTEX) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Open Text Carry?

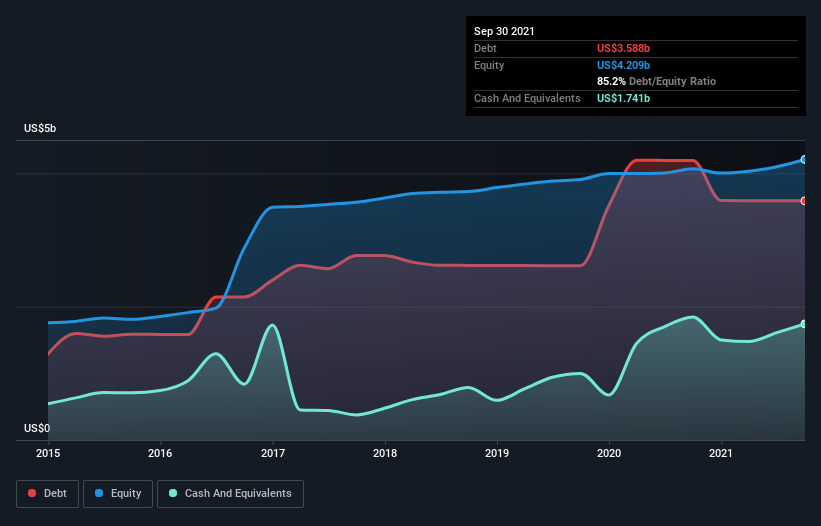

As you can see below, Open Text had US$3.59b of debt at September 2021, down from US$4.19b a year prior. However, it also had US$1.74b in cash, and so its net debt is US$1.85b.

How Healthy Is Open Text’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Open Text had liabilities of US$1.20b due within 12 months and liabilities of US$4.11b due beyond that. Offsetting these obligations, it had cash of US$1.74b as well as receivables valued at US$408.0m due within 12 months. So its liabilities total US$3.16b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Open Text has a huge market capitalization of US$12.9b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Open Text’s net debt is sitting at a very reasonable 1.8 times its EBITDA, while its EBIT covered its interest expense just 5.2 times last year. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. One way Open Text could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 10%, as it did over the last year. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Open Text can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Open Text actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

The good news is that Open Text’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. And we also thought its EBIT growth rate was a positive. When we consider the range of factors above, it looks like Open Text is pretty sensible with its use of debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. There’s no doubt that we learn most about debt from the balance sheet.