Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Mobile TeleSystems Public Joint Stock Company (NYSE:MBT) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Mobile TeleSystems’s Debt?

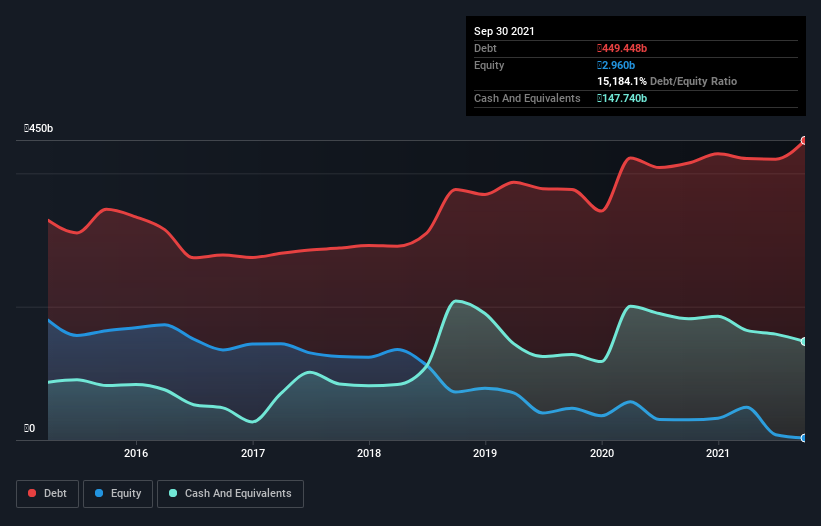

The image below, which you can click on for greater detail, shows that at September 2021 Mobile TeleSystems had debt of ₽449.4b, up from ₽415.4b in one year. However, because it has a cash reserve of ₽147.7b, its net debt is less, at about ₽301.7b.

How Strong Is Mobile TeleSystems’ Balance Sheet?

The latest balance sheet data shows that Mobile TeleSystems had liabilities of ₽395.6b due within a year, and liabilities of ₽556.1b falling due after that. Offsetting these obligations, it had cash of ₽147.7b as well as receivables valued at ₽59.7b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₽744.3b.

This deficit casts a shadow over the ₽491.1b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Mobile TeleSystems would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Mobile TeleSystems has net debt worth 1.7 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 3.3 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. Mobile TeleSystems grew its EBIT by 9.3% in the last year. Whilst that hardly knocks our socks off it is a positive when it comes to debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Mobile TeleSystems’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Mobile TeleSystems created free cash flow amounting to 20% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

We’d go so far as to say Mobile TeleSystems’s level of total liabilities was disappointing. But at least it’s pretty decent at growing its EBIT; that’s encouraging. We’re quite clear that we consider Mobile TeleSystems to be really rather risky, as a result of its balance sheet health. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they say.