Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Griffon Corporation (NYSE:GFF) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Griffon’s Debt?

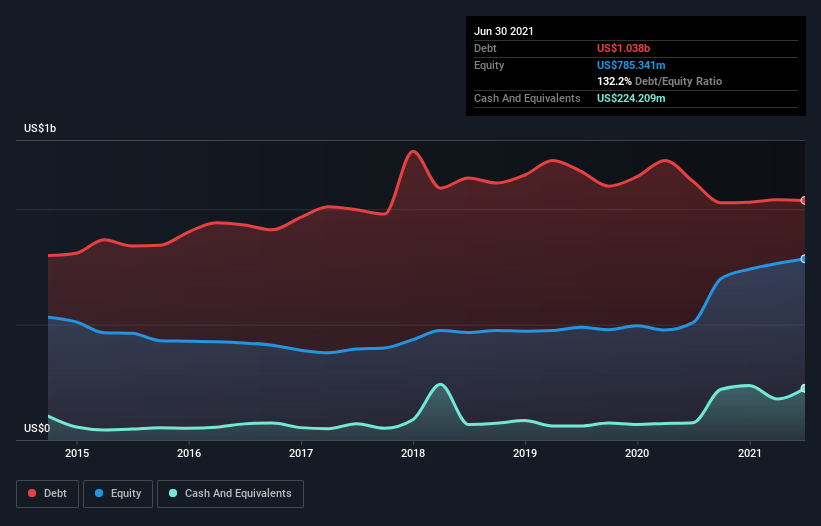

The image below, which you can click on for greater detail, shows that Griffon had debt of US$1.04b at the end of June 2021, a reduction from US$1.12b over a year. On the flip side, it has US$224.2m in cash leading to net debt of about US$814.1m.

A Look At Griffon’s Liabilities

According to the last reported balance sheet, Griffon had liabilities of US$466.5m due within 12 months, and liabilities of US$1.30b due beyond 12 months. Offsetting this, it had US$224.2m in cash and US$437.4m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.10b.

This is a mountain of leverage relative to its market capitalization of US$1.39b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Griffon has a debt to EBITDA ratio of 3.0 and its EBIT covered its interest expense 3.3 times. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. On a lighter note, we note that Griffon grew its EBIT by 28% in the last year. If it can maintain that kind of improvement, its debt load will begin to melt away like glaciers in a warming world. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Griffon can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. In the last three years, Griffon’s free cash flow amounted to 37% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Neither Griffon’s ability to cover its interest expense with its EBIT nor its level of total liabilities gave us confidence in its ability to take on more debt. But its EBIT growth rate tells a very different story, and suggests some resilience. We think that Griffon’s debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There’s no doubt that we learn most about debt from the balance sheet.