Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, e.l.f. Beauty, Inc. (NYSE:ELF) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

What Is e.l.f. Beauty’s Debt?

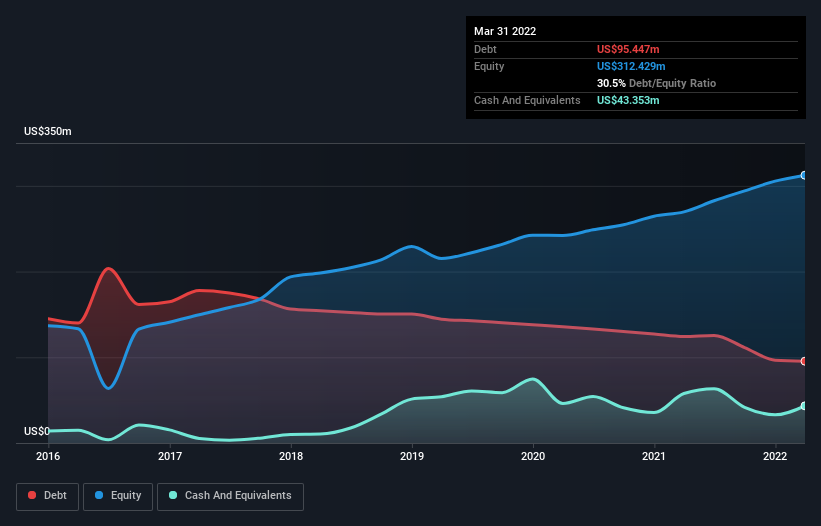

You can click the graphic below for the historical numbers, but it shows that e.l.f. Beauty had US$95.4m of debt in March 2022, down from US$124.3m, one year before. However, it also had US$43.4m in cash, and so its net debt is US$52.1m.

How Strong Is e.l.f. Beauty’s Balance Sheet?

The latest balance sheet data shows that e.l.f. Beauty had liabilities of US$65.0m due within a year, and liabilities of US$117.2m falling due after that. On the other hand, it had cash of US$43.4m and US$45.6m worth of receivables due within a year. So it has liabilities totalling US$93.3m more than its cash and near-term receivables, combined.

Of course, e.l.f. Beauty has a market capitalization of US$1.65b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

e.l.f. Beauty has a low net debt to EBITDA ratio of only 1.0. And its EBIT covers its interest expense a whopping 12.2 times over. So we’re pretty relaxed about its super-conservative use of debt. Even more impressive was the fact that e.l.f. Beauty grew its EBIT by 148% over twelve months. That boost will make it even easier to pay down debt going forward. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine e.l.f. Beauty’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, e.l.f. Beauty actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Happily, e.l.f. Beauty’s impressive interest cover implies it has the upper hand on its debt. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. It looks e.l.f. Beauty has no trouble standing on its own two feet, and it has no reason to fear its lenders. To our minds it has a healthy happy balance sheet. There’s no doubt that we learn most about debt from the balance sheet.